Making Hay Monday - July 17th, 2023

Thank you, Kevin!

Charts of the Week

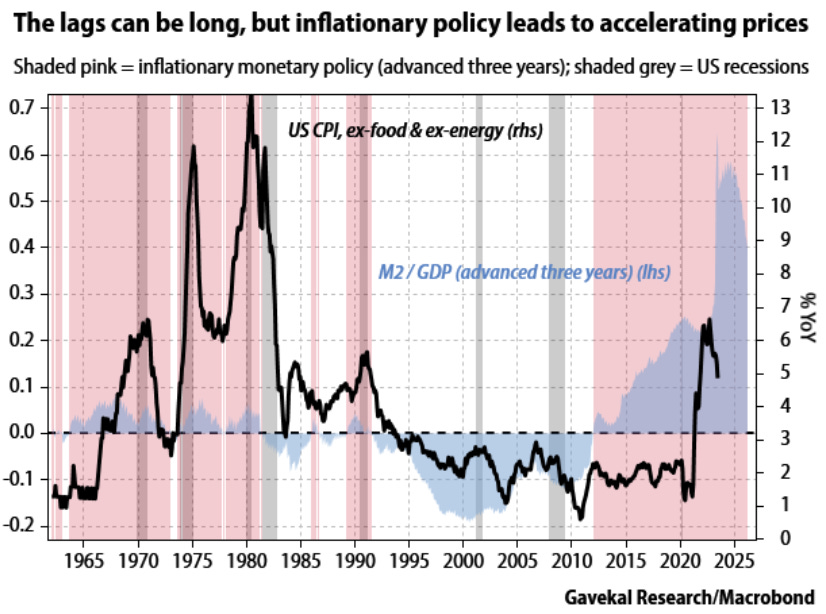

The big economic and financial news last week was the remarkably subdued inflation number reported on Wednesday. This has led to broad euphoria that the dreamed-for soft landing is upon us… that is, if the economy’s wheels even touch the ground. The two charts shown below, however, should serve as a reality check for those who believe inflation is totally in the rearview mirror. These images were extracted from a research note published today by Gavekal’s co-founder, Charles Gave. He is also the father of my great friend and partner Louis Gave.

There is no question that inflation has cooled dramatically from last year’s nearly double-digit levels. Receding commodity prices, especially energy-related, have played a large role in the easing by both the CPI and the PPI (Producer Price Index). But, as Charles describes, there remain trillions of excess liquidity in the system as a result of the unprecedented fiscal and monetary stimulus from 2020, 2021, and even into 2022. In fact, the Federal government is back to running enormous deficits, in the 7% to 9% of GDP range. In dollar terms, the full-year red ink should approach $2 trillion.

One other point to ponder is that June of last year saw a very hot inflation reading. Thus, it was a fairly easy comparison and that’s true for the first half of 2022 overall. July 2022, on the other hand, showed a sharp dropoff. Consequently, the July inflation release coming out next month has the potential to be a disappointment. As a result, taking some profits into the recent broad rally — as opposed to the extremely narrow one that characterized the first five months of this year — might be advisable. However, I continue to like the outlook for more cyclical and value-oriented stocks, such as those that comprise the industrial ETF.

“I would like to explore the idea that the Federal Reserve’s interest rate hikes are nowhere near as contractionary as Wall Street believes, and in fact, might even be expansionary.” -The MacroTourist, Kevin Muir | July 5th, 2023

The Muir Image

The term “mirror image” is a strange one, almost as fluid and changeable as the definition of inflation. Synonyms include “clone”, “duplicate” and “carbon copy”. Yet, when you read the following, you can easily pick up, well, a mirror-image meaning: “The mirror image will be the opposite of the original image.” Say, again?

The ambiguity of this well-known phrase is an ideal fit with the main theme of this Guest Making Hay Monday edition, written by the abovementioned Kevin Muir. Kevin was gracious enough to give me the go-ahead to re-publish his recent thought-provoking — even, iconoclastic — missive. In that regard, my first reaction upon a cursory review was that it was at least partially an endorsement of the monetary policies employed by Turkey’s strongman Recep Tayyip Erdogan. In fact, when I emailed Kevin to ask his permission to republish this note, I somewhat facetiously wrote that my initial impression was that it was pro-Erdoganomics (which shouldn’t be confused with Bidenmonics, at least not yet).

If you didn’t know this, President Erdogan forced encouraged Turkey’s central bank to dramatically slash interest rates, despite that inflation was running hot in 2021. His reasoning was that lower interest rates would lead to lower inflation. Instead, inflation accelerated just a bit — like from around 20% to over 70%.

Ergo, Erdoganomics was a bust.

However, as I nearly always do with Kevin’s notes, I printed a hard copy and read it much more carefully the other day. It may have helped that I was sipping one of my wife’s legendary adult beverages as I did.

Regardless, on the second reading, I got the point — actually, multiple points. One of those is that the reason pundits like me have been wrong about the economy — I’d add, so far — is that we underestimated the power of “stim”; as in, federal fiscal stimulus. It’s a fair position and, in my case, an ironic one. If you go back and read my newsletters from 2021* and into the first half of 2022, my overarching thesis was that the U.S. economy was in an inflationary boom. And, at the time, that was indeed the case.

My master view was that once the Delta and Omicron viruses (remember those?) ran their course, and supply chains debottlenecked, there would be another surge in purchases of big-ticket items, like automobiles and appliances. The trillions of “stimmies” were still in the system and consumers just needed the availability of goods to go on a buying binge, as they had in early 2020 before shortages became acute.

Services, like travel, would also be big winners, in my view. Further, I expected China to get past its lockdowns, which in June of last year didn’t look to be ending anytime soon. Also by that time, I worried that the explosion in energy and agricultural prices caused by the war in Ukraine was likely to cause a deep recession in Europe and possibly mass starvation in parts of the world. Meanwhile, the Fed was frantically playing catch-up to inflation and its aggressive, though belated, tightening campaign was already crushing stocks and bonds. It was a trend that would continue into the fall, creating a negative “wealth effect”. (When people lose a lot of money, they tend to close their wallets.)

Accordingly, I had no reason to doubt the economic textbooks that say dramatically higher interest rates will hurt the economy. The intensifying inversion of the yield curve only reinforced my certainty that a recession was just a matter of time. (However, I did repeatedly write that I was much more confident there would be an earnings recession, in which we are still in the throes).

But, as events have shown, and Kevin describes, soaring interest rates are not, by any means, totally bad news for markets and the economy. This can happen when the Federal government’s deficits blow out, largely due to its own interest costs going postal. That money goes somewhere and much of it winds up in the pockets of America’s savers, particularly the wealthy. As I’ve noted, it’s unprecedented for the government to be running deficits of 7% to 8% of GDP (roughly $2 trillion) when unemployment is close to a record low. Yet, for now, there’s no question that’s been pumping a lot of liquidity into the system.

(One quibble: As I’ve griped before, how healthy is it for nominal GDP to grow at 7% when all of that is represented by deficit spending? I.E., the private sector appears to have gone ex-growth.)

Kevin’s piece is, for sure, a longer read, but if you just want the essentials, especially given my lead-in, skip down to the last 1/3 or so. Suffice to say, a number of the positive liquidity contributors that were activated in the first half of this year are likely to shift into reverse, such as the student loan payment moratoriums. (The incredibly wasteful $20 billion/month of Employee Retention Credits, that have often enriched the already rich, is another program likely to soon get the ax.) The bottom line is: before you conclude the Fed has succeeded in producing Goldilocks: The Sequel, you may want to reflect on his last paragraph. It might just be that the second half of 2023 will be the reverse of the first half. One could even say we may soon be looking at a Muir mirror image.

*Prior to April of 2022, these were published as the Evergreen Virtual Advisor (EVA) and are available on the Evergreen Gavekal website.

To learn more about Evergreen Gavekal, where the Haymaker himself serves as Co-CIO, click below.

If you would like to contact Kevin directly regarding any of his previous or forthcoming work, reach him via email at the following address:

kevin@themacrotourist.com

He’ll be happy to get in touch.

INTEREST RATE HIKES CAN BE STIMULATIVE?

The 'tourist explains why Powell's tightening campaign has been so ineffective

JUL 5, 2023

Lots of folks have been caught off guard by the continued strength of the economy. Back in February I wrote a piece titled “WHY IS THE ECONOMY SO STRONG?” and although there was considerable pushback to the idea that the economy could remain aloft for much longer (don’t forget that back then, most folks predicted recession by this summer), some ideas in that piece have slowly been accepted as reasons for the economy’s resilience.

For example, here is Dan Greenhaus with the guys from “On The Tape” podcast being refreshingly open about his forecast for economic weakness (as a quick aside, I’m a big fan of both Dan and the On The Tape podcast. I would highly recommend them both).

The consumer remains incredibly resilient because the labour market remains incredibly resilient. My assumption was that from back last year, the recession would be sometime in the middle of this year. That now does not seem to be the case (to state that somewhat obviously). Part of the reason, a lot of people (myself included), misjudged the level of excess savings throughout the economy. We underestimated the purchasing power on the part of the consumer — despite consumer sentiment being quite poor (probably because the price of everything is going through the roof), but the money we dropped out of helicopters into peoples’ bank accounts has proven more resilient and allowed the consumer to be stronger for longer.

— Dan Greenhaus

Solus Alternative Asset Management

I chose this segment because Dan articulated much of Wall Street’s expectations and the subsequent realization that fiscal policy changed the game.

But this is something I have been harking on for some time. From my earlier piece:

It seems like at every stage of the post-COVID era, economists and market pundits have underestimated the power of fiscal stimulus.

In March 2020, many pundits thought we were heading into an economic slowdown that would rival the 1929 Great Depression. Much to their surprise, by sending money directly to citizens in the form of fiscal stimulus, the economic fallout was much less than feared.

Then, in 2020/21, stock markets took off in a speculative fervor that was generally dismissed. The power of fiscal stimulus was underappreciated. Sure, the rally might have been foolish, but few economic forecasters predicted the extent of the animal spirits awakening.

And this failure to appreciate the power of fiscal was not limited to markets. The Federal Reserve was blindsided by inflation. After years of not being able to meet their inflation targets, at first, the Fed welcomed inflation. But, the power of fiscal stimulus was misjudged, and next thing they knew, they were way behind the curve with a big inflation problem.

And before you say the bond market understood the power of fiscal, for the past six months, they have priced in a rise in the Fed Funds rate, but then also included an economy that rolls over quickly and causes the Fed to cut rates. The bond market has underappreciated the power of fiscal too.

For the last forty years, the only economic tool the Federal Reserve and the US government has used to revive the economy was monetary stimulus. Encouraging private sector credit creation through lowering interest rates is dramatically different from handing money to consumers directly.

It should probably be expected that markets have underappreciated the power of fiscal stimulus as this has been so rarely done. However, we’re slowly figuring it out, and even the Federal Reserve has highlighted the tremendous amount of consumer savings that continues to support the economy.

However, that’s not what I want to talk about today.

Instead, I want to discuss another possibility that might prove even more difficult to swallow than the previous idea that fiscal policy would make the economy stronger than expected.

I would like to explore the idea that the Federal Reserve’s interest rate hikes are nowhere near as contractionary as Wall Street believes, and in fact, might even be expansionary.

This is by no means my idea. It’s something that former hedge fund manager, Warren Mosler, has been discussing for some time.

However, there are a lot of moving parts, and many times in conversations, nuances get missed, so my goal is to simplify and summarize his argument (while adding my own touches).

Now before we start, if you aren’t familiar with the two ways money is created (with banks creating it via loans or the government spending it into existence), then I would suggest a quick review via “WILL DEFLATIONISTS GET THIS ONE RIGHT?”

Prior to the COVID crisis, almost everyone focused solely on the bank credit creation channel because that was the primary method of influencing the economy. When recessions hit, the Federal Reserve lowered interest rates, which eventually caused folks to borrow more and revive the economy, and when the recovery became too strong, the Federal Reserve increased rates and curtailed borrowing, thus weakening economic activity. This model worked well because the primary source of credit creation was from the private sector.

But that changed in 2020. Instead of the Federal Reserve being the sole influencer of economic activity, the government got into the act with massive fiscal stimulus policies. This proved way more effective than almost anyone predicted.

Yet, it has also changed the nature of the Fed’s influence.

To understand this better, let’s first imagine a world where there is no government debt or deficit. All the credit creation is done through the private sector.

As interest rates rise, it lowers the propensity of private sector actors to borrow money and therefore has a contractionary effect on the economy. The opposite occurs when interest rates are lowered. This is the model that most folks focus on when they think about how the economy works.

Yet, as we have discussed numerous times before, government deficits are expansionary. If the government hands out money (like they did during the COVID crisis), it gets spent and causes more economic activity. It’s also expansionary if the government spends more than it takes in (although it might be less so depending on what the government spends it on, but make no mistake - it’s still expansionary). And if the government cuts taxes (decreasing the amount it is withdrawing from the economy), it is also expansionary.

Deficits are expansionary. Full stop.

Now, there might be financial market movements as a consequence of those deficits that could offset some of the expansionary force, but I think we can all agree that the response to the COVID deficits has shown that effect has been nowhere near as much as previously feared. And I don’t want to get in a philosophical debate about the long-term viability of these deficits as I am not disputing that maybe these policies are unsustainable (without other dramatic changes to our economy that most folks would be slow to accept), but in the short to medium-run, deficits are expansionary.

Given this fact, what is the effect of the Federal Reserve raising interest rates on the government deficit?

Higher interest rates mean bigger deficits. Assuming there is no reduction in spending or increase in taxes to pay for the higher interest rates, the Federal Reserve’s hiking causes larger deficits.

And this might seem counterintuitive, but those are still expansionary.

The government is a net debtor, which means the private sector is a net creditor. The government is spending more money into existence by issuing interest to the private sector. The more the Fed hikes, the more money the government creates to pay the interest.

As the Fed has raised rates over the past year, the deficit has expanded from 3.5% to almost 8% of GDP.

In the private sector, when interest rates rise, a company or person who has borrowed finds themselves with less money for other things. However, governments are currency issuers, so any increase in borrowing costs can simply be spent into existence via deficits.

And here is where it gets even more tricky. In the past, when the Federal Reserve has raised rates, it has had an immediate effect on the cost of the private sector’s borrowing. For example, during the 2004-2006 tightening cycle, many homeowners funded their purchases with ARMs (adjustable rate mortgages) which meant that the Fed’s tightening was almost immediately felt. In this cycle, during the COVID crisis, interest rates were brought to such a low level, and with the Fed’s aggressive QE (which included private sector credit purchases), many consumers and companies locked into funding for a record duration.

This means that the Federal Reserve’s interest rate hiking campaign has had less effect because the private sector actors that would typically be affected are more insulated to interest rate rises.

Let’s review; the Federal Reserve’s interest rate rises mutes private sector borrowing, but this cycle was not driven by this sort of credit expansion. This time, public sector spending led the economy out of the recession. And public sector spending is not constrained like a typical household or corporation, so the increases in interest rates does not force any adjustment in government spending. To make matters even worse, as the Federal Reserve increases interest rates, government deficits expand to fund the extra cost. This increased spending is like a stimulus, making it self-defeating to a certain degree.

Now, you might say, the Fed can’t win; if they raise rates, the increased deficits are a stimulus (minus the decline in private sector credit creation), and if they don’t raise interest rates, the private sector will borrow money as the cost of money is low in real terms.

This conundrum is why the real answer to the Fed’s problem is fiscal.

Back in 2008, Bernanke begged government officials for fiscal stimulus as he righty understood his ability to pull the economy out of the crisis with monetary policy was limited. In 2020, government officials didn’t make the same mistake, but overshot the amount of fiscal stimulus, thereby creating too much inflation. However, instead of admitting their mistake, they have handed the task of controlling inflation over to Powell.

Yet, just as Bernanke was far less effective at creating in inflation during the GFC, Powell will prove much less effective at controlling inflation in the post COVID period. Monetary policy is the wrong tool, but few will admit it.

However, as traders and investors, we shouldn’t focus on what should be, but should make our goal to understand what shall be.

Powell and the market believes that higher interest rates will stamp out inflation. And eventually they will, but the increased deficits from higher rates are having a peculiar stimulative effect few predicted.

Given the fact that Powell’s tightening policy is less effective than expected, this means that the ending tightening level will have to be higher than anticipated. It took way more monetary easing than almost anyone predicted for Bernanke to revive the economy in 2008/9 and it will take way more tightening than most folks expect for Powell to slow down the economy in 2023.

Now, I understand that the COVID stimulus deficit has a different multiplier effect than the “Powell has increased interest rates and the private sector is being paid more” deficit. In the former case, the money went directly into peoples’ pockets and their propensity to spend was large. In the latter case, the spending is going to existing capital holders (ie: wealthier people) and as pundits like to joke; if you give Warren Buffett a stimulus, he doesn’t change his spending - he just buys more stocks with it.

I think this can at least partly explain why financial assets have had such a good first half of the year. Capital holders are getting stimulus cheques through higher interest rates.

And just to add another wrinkle to this already complicated mosaic, usually when the Federal Reserve raises interest rates, the holders of longer duration fixed-income are hurt. However, this time, the COVID QE pulled a lot of duration out of the market, so the Federal Reserve is sitting on a lot of the losses. Again, this makes the Federal Reserve’s interest rate hikes less effective at slowing the economy.

Maybe it’s time?

Although I have explained some reasons why Powell’s interest rate hikes haven’t worked as well as most pundits hoped, they still have an effect.

On the whole, deficit spending is shifting from “real economy direct fiscal stimulus” to “interest payments that will benefit capital holders” (who have a lot less propensity to spend). Therefore, at the margin, we should see the economy do worse and financial markets do better (which I think we are starting to experience).

However, there is something much more important that the market is shrugging off. Recently, the Federal government announced that the student loan payment pause will not be renewed. Therefore, these loans will have to be serviced again.

According to NerdWallet:

For borrowers currently in repayment, federal student loan interest rates have been set to 0% until Sept. 1, at which point they'll start accruing interest again at the fixed rate you got when you took the loans out. Federal student loan payments will resume in October.

The longstanding federal student loan payment pause will expire — once and for all — this fall. Interest will begin accruing on Sept. 1, and borrowers will need to start making payments in October.

There’s no chance of further payment pause extensions, due to a provision in the debt ceiling deal passed by Congress on June 2.

The interest-free payment pause, known as forbearance, began as an emergency pandemic measure in March 2020 under President Trump. Three years and nine extensions later, renewed student loan bills could come as a shock to some of the nearly 44 million borrowers with federal loans. And borrowers who left school in 2020 or later will need to gear up for their first-ever student loan payments.

During the last economic cycle, student loans as a percent of GDP was 2.5%.

Today, that figure is closer to 6%.

The government student loan payment pause (by setting the interest rate to 0%) was another form of fiscal stimulus. That’s going away.

Although the government has no financial need to cut back spending due to higher deficits from increased interest rates, as these deficits grow, politicians eventually adjust their behaviour. Not renewing the student debt pause is a perfect example. Fiscal policy changes from politicians are just slow and much less direct than when compared to the private sector. But politicians are not immune to the increasing red ink from Powell’s interest rate hiking campaign.

The economy has already proved way more resilient to Powell’s hikes than expected, but I suspect we are getting close to where it will start to show in the economic data. Fiscal tightening, like the restarting of student loan payments, will prove surprisingly effective. Taking money out of peoples’ hands is what slows the economy. Unfortunately, Powell’s ability to mute private sector credit creation was the wrong tool for the job as that wasn’t what drove this recovery. Yet, with the slight pulling back on the fiscal lever, and Powell’s extreme tightening campaign, we’re at the stage where in the coming months, the economic surprises will likely be on the downside.

Thanks for reading,

Kevin Muir

the MacroTourist

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions. Receipt of this material does not, by itself, imply that David Hay has an advisory agreement, oral or otherwise, with any reader.

David Hay serves on the Investment Committee in his capacity as Co-Chief Investment Officer of Evergreen Gavekal (“Evergreen”), registered with the Securities and Exchange Commission as an investment adviser under the Investment Advisers Act of 1940. The registration of Evergreen in no way implies a certain level of skill or expertise or that the SEC has endorsed the firm or David Hay. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Please note that while David Hay co-manages the investment program on behalf of Evergreen clients, this publication is not affiliated with Evergreen and do not necessarily reflect the views of the Investment Committee. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Very interesting analysis of the effect of interest rates on the current inflation. See also Lyn Alden’s latest article at lynalden.com for a similar argument that is a bit more accessible for us non-econ majors.

Good analysis...Again, being patient takes some Discipline, something the Markets have never mastered...It's going to be an interesting 2nd half indeed...