Believe her… or your lyin’ eyes?

_(cropped).jpg){kind=link}

“The government doesn’t actually eliminate (bank) failure; it transfers the risk to itself. With enough risk transference, its own solvency and ability to maintain the value of its currency are placed at risk.” -The Wall Street Journal’s Holman W. Jenkins, Jr.

“At particular times a great deal of stupid people have a great deal of stupid money and there is speculation and there is panic.” -Walter Bagehot, one of 19th century Great Britain’s keenest financial minds.

We are interrupting our usual Highlight Reel series schedule to post a further update on the significance of last week’s out-of-the-blue bank runs. One reason is that the stress is now going global. In Europe, Credit Suisse was feared to be the next bank not standing, at least before it scored a $50 billion lifeline from the Swiss National Bank. (To make it easier for those wanting a speed-read, you can just home in on the bold-text sections.)

When it comes to any fractional banking system, where equity is usually only around 10% of the size of its investments (assets) or deposits (liabilities), confidence is essential. Undeniably, faith in the global banking system is being shaken to a degree unseen since early 2009 during the most disturbing days of the Global Financial Crisis. (Perhaps this one will soon be known as “GFC 2.0”)

U.S. authorities obviously recognized the existential threat to the financial superstructure. This was reflected in the nearly instantaneous decision last weekend to provide protection to even uninsured depositors at SVB Financial and Signature Bank. Many pundits are assuming this will extend to the banking system at large should the crisis of confidence intensify.

One doesn’t need to be a conspiracy theorist to wonder about the moral hazard posed by such a radical revamping of the banking industry’s rules of the game. (By the way, the uber-savvy former head of the FDIC, Sheila Bair, is also worried about this aspect, writing in a Financial Times op-ed that it sets a “dangerous precedent” by raising expectations for “future bailouts.”)

For example, if, in reality, all deposits are treated equally, what’s to prevent bank managements from swinging for the duration fences with their investment book? Part of the rescue package was the ability to pledge Treasury securities with the Fed and receive a loan against them based on face value. (This program expires in a year.) Thus, if a long-duration bond (i.e., one with a far-distant maturity) is trading at just 70 but the Fed will lend against as if it was still at 100, why not go long when there’s no penalty for being wrong? As senior research associate at Yale, Steven Kelly, told The New York Times this week: “The Fed has basically just written insurance on interest rate risk for the whole banking system.”

Another moral hazard is that depositors no longer need to exercise care in holding large amounts at a bank. This assumes the FDIC will continue to protect uninsured balances. The Chicago Fed long ago stated: “Uninsured deposits (are) a source of market discipline.” It’s certainly fair to note that there didn’t seem to be a lot of care or due diligence by big depositors with banks like SVB or Signature (the other now-failed bank; in its case, it was heavily crypto focused).

But overall I think it’s reasonable to say most big depositors, be they individuals or corporations, had a tendency to consider the health of their financial institution. Yet, as I wrote on Monday, it astounded me how much money myriad CFOs left at SVB, accepting no insurance and, usually, near-zero yields. It was unquestionably a toxic combination of carelessness and stupidity… the kind usually reserved for senior government officials.

To learn more about Evergreen Gavekal, where the Haymaker himself serves as Co-CIO, click below.

Speaking of that, there is also the extraordinary irony of Signature Bank’s demise. None other than the co-author of the Dodd-Frank Act, meant to protect depositors and taxpayers from inept and greedy bank management teams, sat on its board. Yes, that would be former U.S. Congressman* Barney Frank. This is the same solon who famously and repeatedly raged against the banking industry’s misdeeds during the aftermath of its 2008/2009 near-death-experience. Frankly (pun totally intended, as it was with our earlier Tweet on the same), I’m not surprised. It’s just another in a long list of politicians whose histrionics are choreographed for the cameras — and, of course, re-election campaigns. Yet, I digress…

*Corrected from “Senator”

My overarching point on the deposit guarantees is that there will be consequences. Just like prosperity can’t be fabricated from a printing press — not even the Fed’s Magical Money Machine — a government that’s already bust can’t take on another $7 trillion or so of contingent liabilities without some serious problems eventually arising. Again, this assumes that all uninsured deposits are now de facto government-protected.

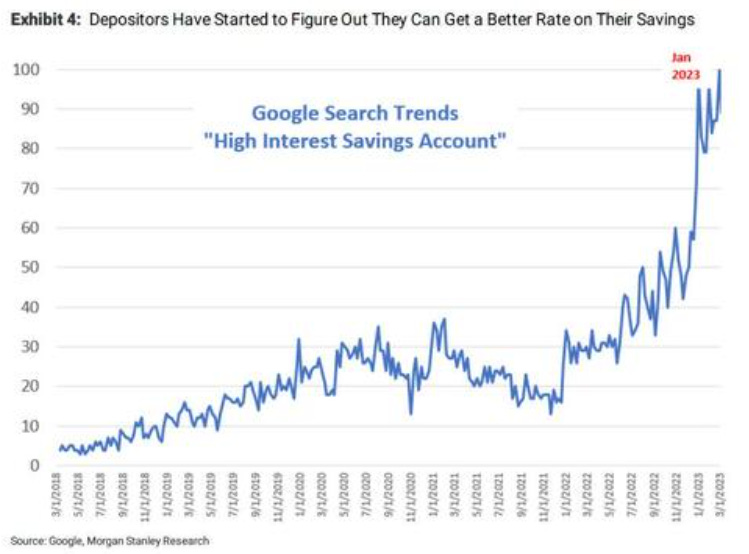

For starters, though the threat of mass bank insolvencies is hopefully off the table, there is still the extreme stress the banking industry’s profitability is experiencing. Despite the new presumed unlimited “limits”, most bank depositors have an aversion to seeing their institution of choice go into receivership. They’re also belatedly waking up to how sloppy it was to have trillions earning next to nothing at a time when T-bills were paying 5%. (Those days may be gone, but 4% plus is still achievable.)

The willingness of countless depositors to accept less return and higher risk versus the safety and 4% type return on ultra-liquid government money market funds continues to astound me. In fact, it’s the craziest thing I’ve seen in my 44-year career. And that has overlapped with some of the most bizarre events in financial market history.

As I wrote on Monday, this means trillions are moving into a much less energetic status with a profound affect on money velocity. Due to the urgency to meet our publication deadline, I glossed over what that really is in my last note. It essentially is a measure of the speed with which money is circulating throughout the financial system. Bank deposits are considered “high-power money” because they can be lent and re-lent multiple times. Money placed in government securities doesn’t have anything close to this type of multiplier.

America’s most famous economist of the early 20th century was Irving Fisher. Admittedly, he did his once-stellar reputation irreparable harm by rationalizing the insane stock bubble of the late 1920s. (In mid-October of 1929 he opined: “Stock prices have reached what looks like a permanently high plateau.” Two weeks later, they cataclysmically fell off that plateau, ushering in the global Great Depression… and Adolf Hitler.) Yet, his body of work on the economy and interest rates has stood the test of time.

One of his most enduring formulas was almost up there with Einstein’s e = mc², at least from an economics standpoint. In his case, it was MV = PT. “M” stands for the money supply, “V” = velocity, “P” = prices and “T” = the number of transactions. Prof. Fisher’s assumption back then was that velocity was a constant; i.e., it didn’t change. Even the greatest economist (in my opinion) of the second half of the 20th century, Milton Friedman, agreed with this; the reality was that, for many decades, velocity hardly varied at all. (“PT” in the above equation roughly equates to nominal GDP, or the total amount of economic activity.)

In the wake of the Global Financial Crisis, velocity plunged. This is why all those trillions the Fed fabricated to stabilize the system in 2009, and for years to come, didn’t produce the high inflation many feared when the first quantitative easing (QE) began. In fact, falling velocity was one of my main counterarguments against the inflationistas 14 years ago, as I conveyed via my newsletters in those days.

Of course, after the Covid panic it was a very different story. The Fed whipped up more trillions, this time almost overnight. More significantly, the U.S. government sent much of that directly to consumers and businesses. This caused velocity to turn up, and inflation did as well, vaulting to its hottest level since the early 1980s.

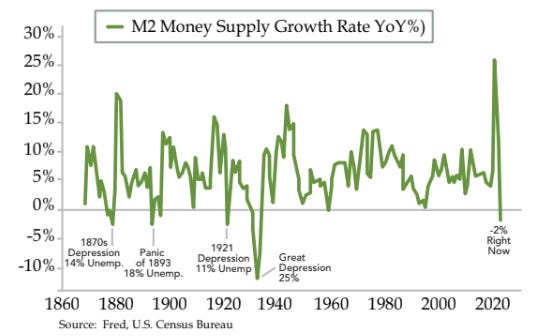

Now, however, I’m convinced velocity is set to turn down once again, likely dramatically. This is because, as I wrote on Monday, when there are trillions moving from bank deposits into government securities, the above-referenced multiplier effect goes down dramatically. Thus far, few others seem to share my concerns, other than Gavekal’s resident monetary expert Will Denyer. If we’re right, that — combined with a U.S. money supply that is contracting in real terms for the first time since the 1930s — is a nasty double-whammy for the economy.

Earlier this week, I listened to the Bond King Jeff Gundlach offer up his take on the sudden financial paroxysm. While he didn’t get into velocity, he did express his belief it will be at least disinflationary in the near-term and accelerate the start of the recession. Those are two views I share. But then he went on to say he believes the bailout will create more inflation long-term. His basic take is that this is decidedly an inflationary policy in the fullness of time.

Gundlach did not offer his reasoning for that, but I’d hazard to guess it relates to the opening quote by Holman Jenkins, Jr. The federal government’s response to this mini-panic is, in my mind, a sneak preview of what will happen with QE. In other words, if a recession is looming — particularly, a nasty one — the Fed is nearly certain to shift from QT (shrinking its balance sheet), back into QE (expanding it).

Actually, the emergency bank loans being extended right now are already having that impact. These would seem to be a real-world refutation of Janet Yellen’s assurances that the U.S. banking system is healthy.

Deutsche Bank’s prolific Jim Reid nicely summarized the chain reaction that has been playing out in a note this week. To wit: “Although the SVB scare is a symptom of the problem, it’s probably not the main event. It is disproportionately exposed to tech and private capital, both of which are struggling. However, it would be hard to say this boom-bust cycle is deviating too far from the script at the moment. That being…too much stimulus -> very high inflation -> aggressive central bank hikes -> inverted curves -> tighter lending standards -> recession.” With the stock market still firmly in denial that a recession is pending, it will be a serious problem if he, Gundlach, and yours truly are right.

So, what are the investment implications of all these developments? First, though tech stocks have been rallying in the wake of the SVB blowup, I think it’s another reason to be underweight this sector. (Note, “underweight” doesn’t mean “zero” weight.) Valuations remain extremely generous, if not ludicrous, for many tech stocks, despite the fact that some have come down to reasonable price points. SVB was a key lynchpin in the tech ecosystem and losing it has to be a negative. Even if you say that companies like Google don’t need to rely on bank financing, certainly many of its underlying customers aren’t as fortunate.

Because tech has been America’s most vibrant sector, additional headwinds are also not great news for the economy at large. As you’ve no doubt noticed, layoffs are going viral in Silicon Valley. Moreover, a stressed banking system means less lending to businesses, particularly smaller enterprises, which generate some 2/3 of employment growth. Ergo, expect job losses to fan out beyond tech and financial institutions.

Next, if the dollar is in a long-term downtrend, burdened as it is by the nearly incomprehensible amount of liabilities its issuer faces, investments that benefit from its weakness should do very well over time. That would include almost all hard-asset-type securities, including the now deeply out-of-favor energy sector. The recent correction has restored considerable value to oil-and-gas-related issues, and they weren’t expensive even at the highs of late last year. Dividend yields also are often extremely attractive.

With financials, I’d be shifting away from pure banks and into financial entities that aren’t as exposed to rising funding costs, portfolio losses and accelerating problem loans. America’s original discount broker looks attractive in that regard, even though it isn’t immune to these negative trends.

Some of the mortgage REITs have come down hard and may be worth a small buy at this point. If the Fed is done hiking and the yield curve is poised to un-invert, that should be a boon to this group. As a reminder, if history is any indication, it’s when the yield curve shifts from inverted back to its normal slope (short rates lower than long rates) that a recession is imminent. Because nearly all of their assets are government securities, they tend to do well during recessions. Historically, they are further aided by a normalizing yield curve (i.e., short rates falling much faster than long rates).

While Treasury bonds in the two- to five-year maturity range have been on fire in the wake of the SVB disaster, should they move back up in yield by a considerable amount, those would be a decent destination for some of your capital. However, 10-year and over-maturity Treasury bonds in the 3½% range still don’t strike me as appealing, given the longer-term inflation risks.

To close, it’s clear to me that all the recent convulsions are consequences of the bursting of Bubble 3.0, the biggest bubble of all time. One of the biggest victims of this is likely to be commercial real estate. Smallish banks provide 80% of lending to that sector. For those readers who are directly and indirectly exposed to the commercial property market, I’d suggest you be on high-alert. If you think it’s bad now, just wait a few months. It might soon feel like déjà vu 2009 all over again.

Your writing is entertaining on top of being very insightful. I always look forward to your Monday and Friday releases. Thanks for taking your valuable time to educate the masses...OK maybe not masses but at least those of us who care.

I second James comment - you’re never too old to learn and never to old to learn from those smarter in a given field - Ty Haymaker