Making Hay Monday - November 25th, 2024

Wishing you all a very happy Thanksgiving weekend!

Hello, Readers, and Happy Thanksgiving Week!

Today’s MHM is formatted along the lines of an extended Trading Alert. We’ve also updated the Asset-Class Lists because our MHMs just aren’t complete without those. Like a Thanksgiving meal without the stuffing – unthinkable.

If you’d like to see more Trading Alert content like this from Haymaker, let us know in the comments section. Your input means a lot to us.

We’re looking forward to finishing up the year with some actionable ideas and 2025 forecasts. Before getting that underway, let’s all have a beautiful week with those we love.

The Haymaker Team

The U.S. stock market has been outperforming the rest of the world for so long that this appears to be a permanent condition. Perhaps that is true but the degree to which it has continued to leave the planet’s other equity markets in the dust now appears to be a function of a uniquely American bubble.

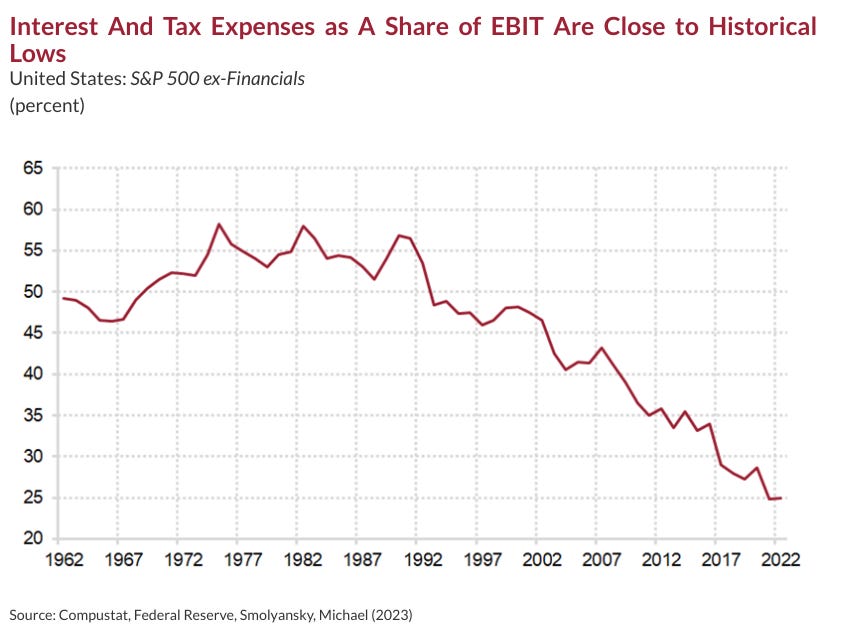

An obvious reason U.S. shares have been star performers in recent decades, and especially the last 10 years, was due to far superior relative earnings performance. It is assumed that the profits explosion by Magnificent Seven type companies was the main driver of that. To a degree, such a perception is likely valid. However, the main force behind America’s earnings boom over the last 30 years has been declining interest rates and taxes. Real profit growth has doubled over that period versus the prior three decades. This is despite much weaker GDP growth, particularly since 2000 and also slower real operating income increases (i.e., before taxes and interest). With Donald Trump vectoring to slash the corporate tax rate to 15% and the Fed beginning an interest rate cutting cycle, perhaps this amazing trend has further to run. Based on current U.S. stock valuations, it better.

“In fact, in many ways, demand for leverage has never been greater than it is today despite the fact that it has rarely if ever been more expensive. This points to a degree of euphoric speculation that is both exceedingly rare and highly dangerous…another irony: while retail investors are gorging on leverage like never before, the smart money has simultaneously become more defensive than ever before.” -Jesse Felder, The Felder Report

Haymaker Note: We have some specific trading recommendations in this Making Hay Monday that are only available to our paying subscribers. At this gratitude-appropriate time of the year, we would be most thankful if you would become part of our effort to help investors protect their wealth during what is likely to be a chaotic, but opportunity-filled, second Trump administration.

Power Punchers

With the passage of two years’ time, it is easy to forget how painful 2022 was for financial markets. That was the year which saw the popping of what this newsletter has long referred to as Bubble 3.0. In fact, that orgy of speculative excess caused the aged Haymaker to publish a book with that title in early 2022.

At this point, for a long list of U.S. stocks, though, it’s definitely a case of convenient amnesia. The 70% to 80% evisceration endured by a multitude of equities that had been trading at insane valuations at the end of 2021 has mostly been forgotten. 2024 is almost certain to be the second consecutive 20% plus return year for the S&P 500. Surprisingly, the S&P 500 is actually ahead of the NASDAQ 100 so far this year but both have gained in the neighborhood of 25%, a very nice zip code indeed. However, considering the boost the “Naz” has received from Nvidia, which has had less of an impact on the S&P, that’s a bit surprising.

It is worth pondering what has driven this exceptional performance. Has it been earnings? To an extent, yes. They are currently running 8% to 9% higher than a year ago, but that’s much lower than the approximate 40% total return (i.e., including dividends) for the S&P since 10/1/2023.