Making Hay Monday - May 20th, 2024

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day's financial fray.

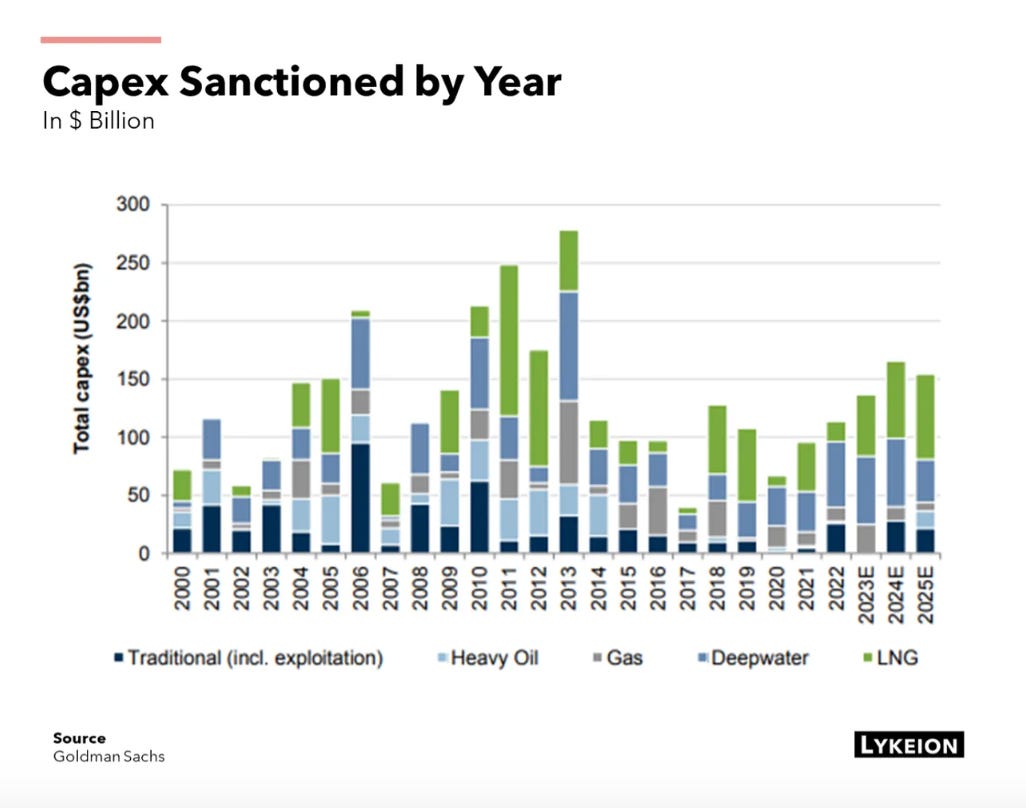

Charts of the Week

Trader Ferg does it again! In the above visual, he came up with one of the most revealing factoids I’ve seen on energy in a very long time. As closely as I track that sector, I’m embarrassed to admit I wasn’t aware of the reality that spending on liquefied natural gas (LNG), mostly for export, has amounted to almost half of all capital spending by oil and gas companies. Due to the fact that, per the chart on the right, overall cap ex has done a cliff dive is worrisome enough. The energy industry is clearly putting much more emphasis on returning capital to shareholders than on searching for new oil and gas. That is a point I’ve repeatedly expressed and it portends future acute shortages. Factoring in how much of that shrunken capital spending has gone into building out the LNG infrastructure, to send America’s gas offshore, makes this grave situation even more dire.

The contrast between Corporate America’s flush finances and those of its dead-broke (and getting deader) government couldn’t be starker. It is important to point out that much of that cash hoard is held by the S&P 500’s ten biggest companies. There are, of course, myriad companies that are somewhere in between those whose balance sheets are brimming with cash and those whose high debt levels mean they are being increasingly squeezed by high rates. The latter are particularly exposed as their low-cost debt, taken out in 2020 and 2021, begins to come due. You are likely to hear more about the impending “maturity wall” facing these highly leveraged entities. Defaults are already rising sharply and that’s likely to continue over at least the next two years as more companies literally hit the wall.

“Fiscal irresponsibility is going to end up killing us all.” -Michael Gayed, author of the Lead-Lag Report.

Champions

A Much-Needed Sigh Sy of Relief

It is hard to believe that as recently as February, the gold miners were on their heels. Since then, they’ve been more like hell on wheels. Both the senior and junior gold miner ETFs have experienced rousing rallies. Each is now up over 20% for 2024, smoking the S&P’s return. When we published our February 20th Making Hay Monday (MHM), they were at 27 and 32½, respectively.

Here's what I wrote on the junior miners at the time:

It’s time to formally upgrade junior gold miners back to Champion status. There are ETFs out there that do provide access to this sub-sector. Part of my logic for doing so is that companies of this size are the most probable takeover targets for their larger competitors, like Agnico Eagle, Barrick, and Newmont.

* * *

The current trading level of the junior gold miners looks to offer an attractive entry point. They are down about 25% from their 2023 highs and are barely above half of where they topped out in 2020. If you go further back, to 2010, they have tanked by roughly 80%. In other words, pretty much what happened to the NASDAQ after it did its moonshot in early 2000.

In our February 12th Making Hay Monday, I identified the Super Investor we featured in our December 15th, 2023, edition, Sy Jacobs. Sy graciously let me use his name in that follow-up issue when I congratulated him for how well his two precious-metals related ideas had held up in a tough market for gold and silver plays. The two names he had given me strong buy cases on back in mid-December were A-Mark (AMRK) and Sprott, Inc. (SII).

At the time, both were down minor amounts, particularly for anyone who had taken my suggestion to be careful about the price they paid. This was because they had both rallied sharply as I was writing the 12/15/23 MHM. (Also in the follow-on note, I covered an insurance company, Chubb, due to the fact that Sy was also bullish on property/casualty stocks. You may have seen what happened last week with CB and Berkshire Hathaway. The Barron’s article below is one that all who are interested in, or owners of, Chubb should check out. We’ve excerpted some key points which you can find at the end of this post.)

Similar to the miners themselves, both AMRK and SII have been en fuego since mid-February. Certainly, after the surge they’ve had its prudent to be much more reserved about adding to either of them. Long-term, though, the stories remain intriguing.