Making Hay Monday - June 17th, 2024

High-level macro-market insights, actionable economic forecasts, and plenty of friendly candor to give you a fighting chance in the day's financial fray.

Charts of the Week

Longtime Haymaker readers will have seen our repeated warnings regarding poor “market breadth” (or market “halitosis”, as we usually put it), and more specifically, the lack of breadth at work in the present market. To quote David Rosenberg, from whose Breakfast With Dave publication we’re borrowing the above visual:

Market breadth remains an issue, with the “internals” not as healthy as perceived and with concentration risk remaining high (and rising) — note that the ratio of the equal-weighted S&P 500 relative to the cap-weighted index is down to its worst level since March 2009.

Whenever we start hearing well-informed negative comparisons to the economy of 2009, we know to pay attention. There’s little question that the AI-fueled “gold rush” of the past year or so is contributing to the narrow market.

Similar to David Rosenberg’s work, the Brogan Group, which specializes in analyzing money flows into and out of the market, as well as sectors, told its clients today that the percentage of stocks outperforming the S&P 500 is now at the lowest level on record. (They did go on to note their money flow analysis remains positive.)

The Haymaker take is that either market breadth improves soon or money flows are likely to deteriorate. There have been some instances in recent years where the rally has been sustained by broader participation. Let’s hope that happens again…and quickly.

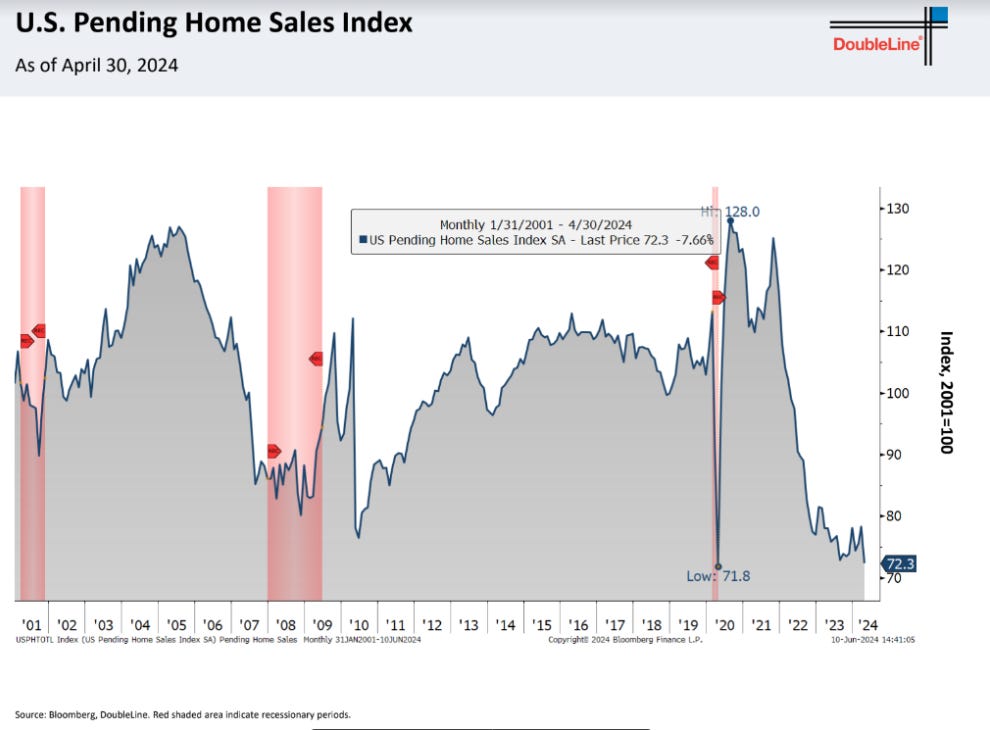

Later this month, we’ll be running a piece in anticipation of the Presidential Debate scheduled for June 27th*, which, Biden’s attempts at a quip notwithstanding, does not fall on a Wednesday. We’ll be covering not what distortions to expect specifically, but what political topics are most vulnerable to such distortions. Of those, housing and its rippling economic implications are near the top of the list. It’s the sort of topic politicos on either side of the aisle love to address because accountability and accuracy are easy to skirt when a subject is so complex. But maybe it needn’t be. Taken together, the doubled-up DoubleLine charts above tell a grim story of where housing purchases are (in the basement) and what new homebuyers can expect if they’re “lucky” enough to land a set of house keys (the presently crushing cost of ownership).

*Corrected from original post, which indicated the debate was scheduled for two weeks later.

“Unless Anglo-American foreign policy is successful in replacing Putin with a puppet who only sells oil and commodities in (U.S. dollars)…then the IEA’s oil demand outlook for 2030 is likely to be very wrong.” -Forest for the Trees author Luke Gromen

Crude Calculations, Continued

Champions

In the April 1st, 2024 Haymaker edition, the International Energy Agency (IEA) multi-decade miscalculations of the demand for crude oil were highlighted. As discussed at the time, the IEA’s constant and immense underestimation of oil consumption, along with the less dramatic but still significant overestimation of supply, has produced a tracking error literally in the billions of barrels over the years. Frankly, the IEA’s forecasting record is so bad it makes the Fed’s look downright clairvoyant.

Cornerstone’s Mike Rothman has been in a running battle with the IEA going back to the late 1990s. He has consistently been vindicated with the passage of time. Lately, certain members of Congress have joined the fray. Several have written the IEA to express their displeasure with its inexplicable conveyance of grotesquely flawed data. One of their key criticisms is that by continually brainwashing informing the world that there is a chronic oversupply of oil, it creates a disincentive to make the long-term investments necessary to support the on-going growth in demand for crude.

A crucial element in the IEA’s dogma that the need for oil is peaking has to do with electric vehicles (EVs). Yet, the reality is that, per Statista, “… the unit sales of Electric Vehicles market are anticipated to reach 17.07m vehicles units by 2028.” This is versus almost no sales 10 years ago. Despite that, the demand for oil has continued to increase. As noted in numerous prior Haymakers, this is totally a function (actually more than) of the rising appetite for oil in developing countries. Among developed nations, crude consumption has in fact declined.

Last Wednesday, the IEA did it again. Media sources around the world were blaring that by 2030 oil will be massively oversupplied. Here’s a typical headline, in this case from the Financial Times: “Energy watchdog foresees ‘staggering’ oil glut while producers keep pumping”.

If the IEA is the planet’s energy watchdog, it does beg the question who is watching the watchdog. Until very recently, Mike Rothman has been almost alone in his challenges. Lately, though, in addition to the Congressional push-back, others such as Luke Gromen and the prestigious energy research firm, Goering & Rozencwajg*, have joined the cause. But, illustrating their minority status, I didn’t see a single article about Wednesday’s sensational IEA declarations disclosing the agency’s abysmal forecasting track record. As usual, the mainstream media simply laps up their misguided reports.

What the IEA is overlooking, in addition to other facts, is that the growth rate for EVs is slowing. It did concede that even a modest downshift in their EV demand forecasts could throw off their conclusions.