Making Hay Monday - June 16th, 2025

On the Asian Anti-Contagion

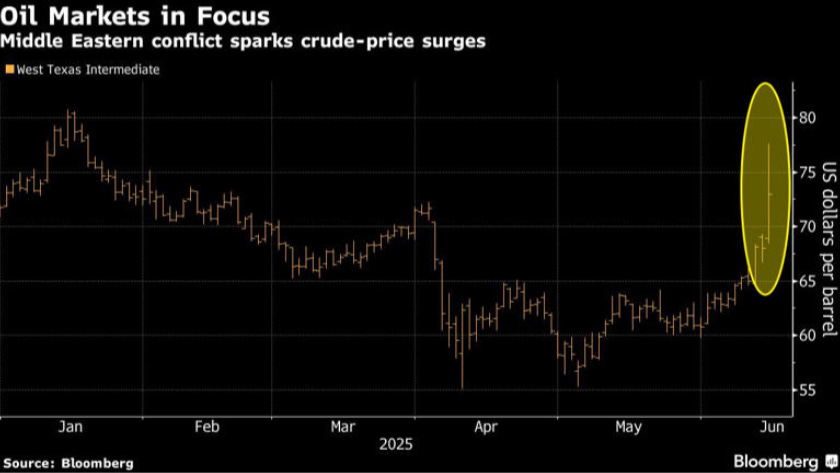

Despite that the odds were rising that Israel was preparing to launch an aggressive attack on Iran, at the start of June oil was trading as if geopolitical risks were non-existent. Per the above chart, that’s clearly no longer the case. With the latest quote for West Texas Intermediate (WTI) around $72, after hitting $77 in weekend trading, the oil market has understandably experienced one of its most rapid price eruptions since the 2022 Russian invasion of Ukraine. What isn’t understandable is how complacent energy traders were just two weeks ago. It did create an opportunity for contrarian investors who were tracking Israeli preparations and Iran’s prevarications in its nuclear negotiations with the U.S. Usually, when oil surges energy stocks rise even more but, thus far, that’s clearly not been the case. Once again, independent-thinking investors should consider accumulating oil and gas-related securities in the event that the Israel/Iran conflict escalates. This could potentially include a desperate attempt by Iran to close the Strait of Hormuz. Twenty percent of the world’s oil supply passes through shipping lanes that are as narrow as two miles across in each direction.

Even before the latest war in the Mideast roiled oil markets, inventory levels at Cushing, Oklahoma, America’s primary crude-storage facility, were close to 20-year lows. Yet, the prevailing narrative was that there was a glut of oil and that prices could continue falling, even after they tumbled into the upper 50s. What may have been overlooked, along with many other supportive considerations, was that OPEC might have been increasing production in the event that Israel went after Iran’s energy infrastructure.

Over the weekend, Israel hit Iran’s South Pars facility, one of the world’s largest natural gas fields, which it shares with Qatar. South Pars also produces natural gas liquids which are at least partially oil alternatives, further tightening the crude market.

"There are four kinds of countries: developed countries, underdeveloped countries, Japan, and Argentina." -Simon Kuznets*

“Elevated spare capacity and significant recession risks tilt the odds for oil prices downward, despite relatively tight spot market conditions.” -Goldman Sachs analysts, Daan Struyven, earlier this month while also projecting a global oil market surplus of 800,000 barrels per day in 2025 and 1.4 million barrels per day in 2026, driven by OPEC+ easing supply curbs and sluggish demand growth. (Source: Perplexity)

Special Message

Last week’s Israeli attack on Iran is obviously a dramatic development, perhaps the most significant of 2025. Per our May 28th Trading Alert, it should not have been a surprise.

What is somewhat surprising is how little U.S. stocks are trading off given the potential for escalation. It is also superficially perplexing that energy equities are experiencing a feeble rally in the wake of this news. But perhaps that is another reflection of the total disregard with which they have long been held by most investors.

With the energy sector representing just 3% of the S&P 500’s market value, there is the potential for significant amounts of capital to flow in its direction. The minuscule market cap could mean that a minor reallocation — say, out of the tech sector — might create a disproportionate rally in energy equities. This could be similar to what has happened to gold mining shares this year. Both the senior and junior gold miner ETFs, GDX, and GDXJ, have risen over 60% in 2025.

As with energy, it’s safe to say that most U.S. investors have had minimal, perhaps even zero, exposure to the gold miners. Accordingly, precious few have benefited from the muscular rally by precious metals producers. It’s hard to chase the gold miners after such a spectacular run, but oil-related issues may give investors another shot on goal with a sector that has minimal downside and resounding recovery potential.

Asian Anti-Contagion

Approximately 28 years ago, one of those butterfly-flapping-its-wings events occurred. In this case, it wasn’t in Brazil but, rather, a different emerging nation: Thailand. And it didn’t create a weather disturbance, the mythical tornado in Texas but, instead, what would become an eventual global financial hurricane of the first order.

When Thailand acquiesced to market forces and allowed its currency to collapse in July of 1997, it triggered a chain reaction of chaos in other Asian countries. This soon became known as the Asian Contagion, a nicely catchy term though its implications were anything but nice. Indonesia, Malaysia, and the Philippines saw their currencies plunge shortly thereafter.

By October of that year, even South Korea was on the brink of defaulting on its government debt. Its vast U.S. dollar-denominated liabilities became much greater almost overnight thanks to the collapse of its currency, the won, which suddenly became wan in the most extreme sense of the word. Lest you think “collapse” is an exaggeration, its value, in U.S. dollar (USD) terms, vaporized by two-thirds. The S. Korean stock market was cut in half and unemployment roughly tripled to 8.7%.