Making Hay Monday

A key reason higher interest rates have not caused more stress for Corporate America is that, unlike the U.S. government, it used the pandemic-induced interest rate implosion to refinance its outstanding debt at low yields. This was similar to what millions of homeowners did with their mortgages. The corporate debt extensions were much shorter-term than with 30-year mortgages, however. Now, a multitude of companies are facing the so-called “maturity wall” where the number of their bonds coming due literally goes vertical. This reality seems to be escaping investors who, collectively, are close to as bullish as they have ever been on U.S. stocks. Similarly, Wall Street is projecting 14% earnings growth for 2025. This is despite the rapidly rising cost of capital and a global economy that looks increasingly squishy, if not recessionary.

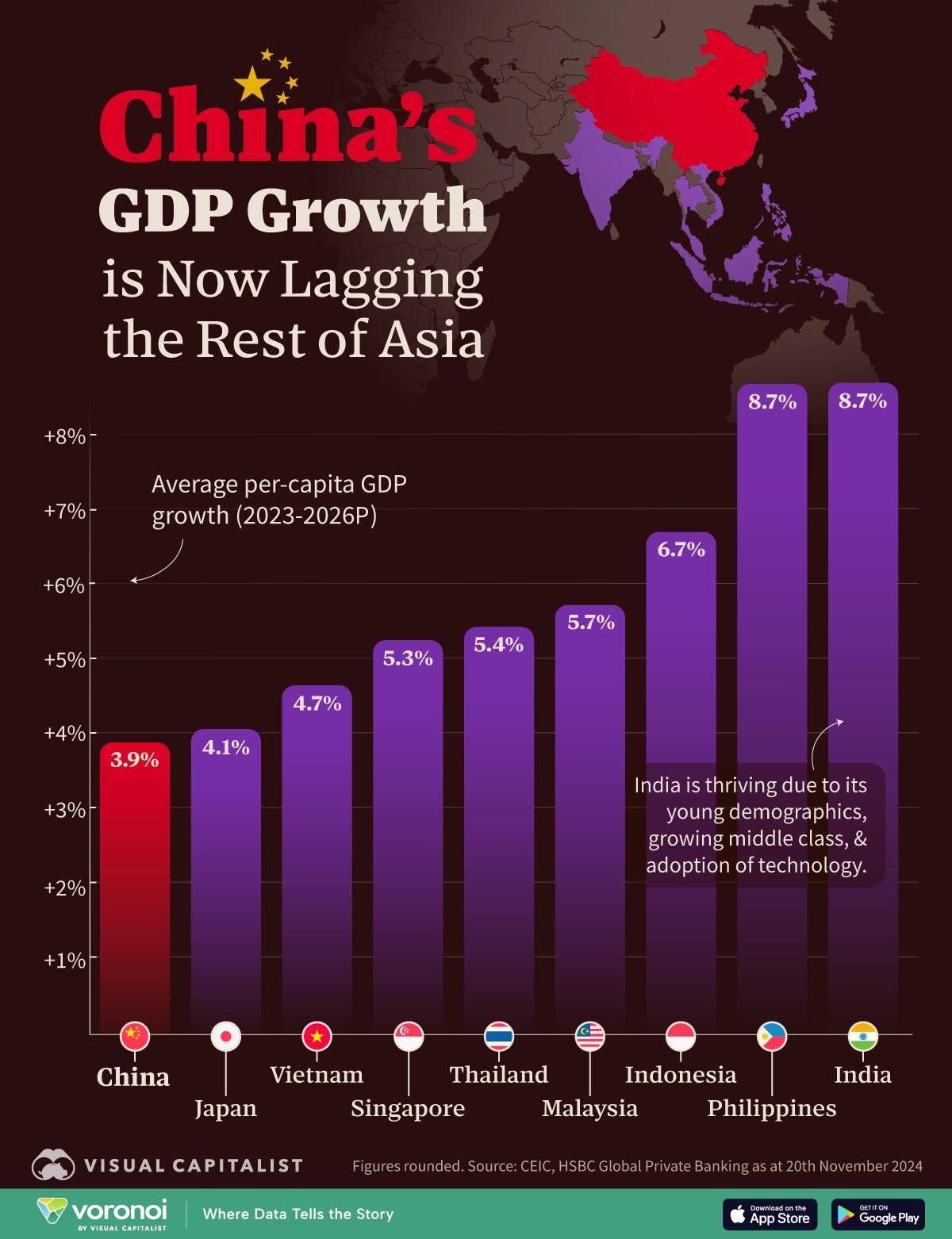

Asia has long been the world’s primary growth driver. China, of course, was the main engine behind that for many years. However, under the iron-fist rule of Xi Jinping, its once-roaring economy has decelerated down to developed-world levels. It is now lagging even Japan. At this point, it may not be unfair to refer to it as “the sick man of Asia”, a pejorative once applied to Germany with regard to Europe. Of course, based on the disastrous impact of Germany’s energy policies, kneecapping its long formidable industrial base, it is also once again an economic basket case.

“There is some crazy stuff going on in a stock market that is trading in a bubble by any measure (other than the perspective of Wall Street which, as we all know, is in the business of convincing people to buy things they shouldn’t buy).” -Michael Lewitt, publisher of The Credit Strategist

The Yield Shield

For those who think the oversold bond market may soon rally, a high-octane way to play that potentiality would be with those specialized real estate vehicles known as Mortgage REITs or mREITs. By cherry-picking individual names, you can easily attain yields in excess of 10% such as with the only member of this sub-sector that is covered by Value Line.

Importantly, these are legitimate yields; i.e., they are not inclusive of return of capital, an income-boosting ploy to which many funds resort. Too often, retail investors simply look at the yield a security is generating, particularly with funds, and assume it is from net-earned cash flow. Frequently, that’s not the case and a reliance on return of capital to support the yield can, and often does, eventually lead to payout cuts.

When a security offers a yield as high as 10%, it’s safe to assume there is a decent amount of risk that goes with the high income. That is indeed the case with mREITs. As this newsletter has pointed out in the past with regard to this niche of the publicly traded real estate market, mREITs are essentially leveraged bond funds. In this case, the bond type instruments are actually mortgages, mostly of the government-guaranteed variety.