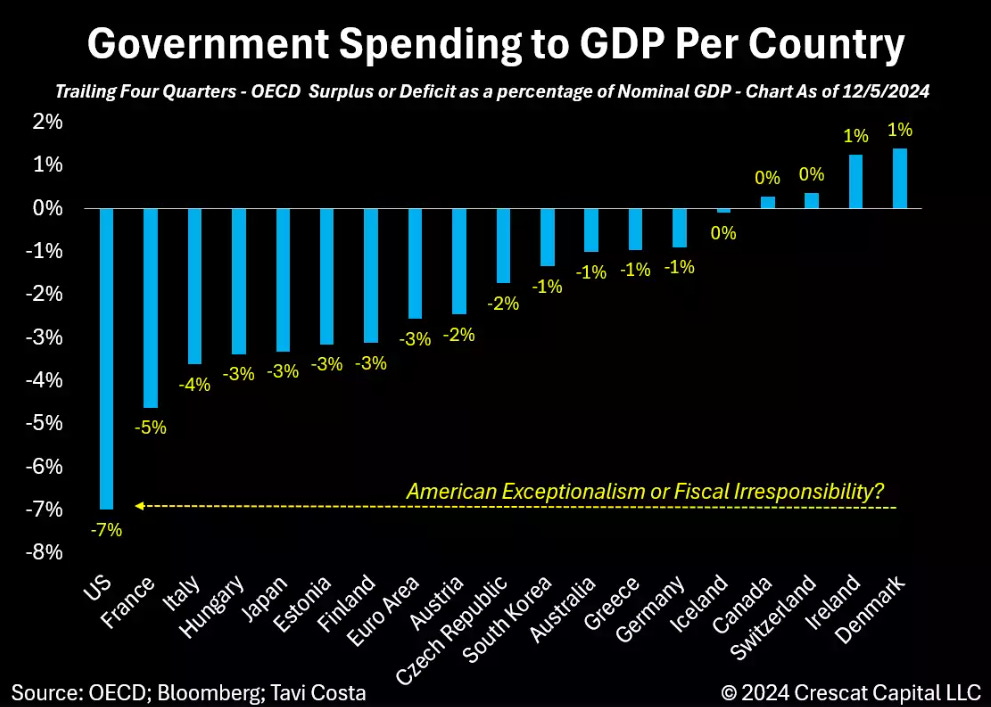

While almost all Americans with a functioning cerebral cortex are aware that the U.S. government is running insanely large deficits, it’s illuminating to see this in the context of the rest of the world. Frankly, it is simply inexcusable that the world’s leading superpower makes France and Italy look like paragons of fiscal probity. Bulls on both the U.S. economy and the stock market should be aware that there is a distinct possibility the incoming Trump Administration will seek to take the pain of slashing government spending down to more normal levels, like 3%, early in its term. Although this should be a distinct long-term positive, it is likely to almost immediately retard economic growth. On a related note, it’s an interesting thought experiment to ponder what Germany’s economy would look like if it was running a 7% deficit to GDP and America somehow managed to lower its federal red ink to 1%. While it’s hard to know for sure, it is a low-risk bet that Germany would no longer be regarded as the “sick man of Europe” and America’s long delayed recession would be in full swing.

One of the Trump administration’s most pressing goals is to reshore manufacturing back to the U.S. In doing so, it hopes to raise living standards for blue collar workers, millions of whom have done a profound pivot to the GOP (or at least Trump’s incarnation of the Republican party). One “yuge” obstacle in doing so, however, is the reality that in dollar terms, the real cost of U.S. manufacturing wages has soared versus America’s main trading partners over the past 15 years. The yen is particularly glaring in this regard. This underscores how crucial it is for Team Trump to drastically reduce the U.S. dollar’s value. To that point, there are rumblings of a new “Plaza Accord” which produced a precipitous decline in the dollar’s exchange rate back in 1985.

“What is different today relative to the fall of 2022 and fall of 2023 is the positioning cycle is currently in an extreme bullish condition…Investor positioning was in an extreme bearish condition in the fall of 2022 and fall of 2023. What is also different…is risk assets have not aggressively priced in the reduction in liquidity…” -42 Macro’s Darius Dale

A New Friend for the Yen?

At this point in time, I’m not sure even James Taylor would warble “you’ve got a friend” when it comes to Japan’s long-battered currency. Even when it enjoyed a mammoth rally last summer, it was almost totally due to short covering by highly leveraged hedge funds rather than any true fondness for the yen’s prospects.

As a refresher, the reason that sophisticated investors short the yen is to borrow at rates barely above zero. Although Japanese interest rates have been rising sharply, they remain sub-1% on the short-end of the yield curve. (As we will soon see, it’s a much different story further out on the maturity spectrum.) Accordingly, it continues to be very attractive for hedge funds to borrow in yen to finance higher-return overseas investments and/or speculations, like meme coins where the profits are lush and almost instantaneous.

The Bank of Japan almost certainly emboldened this rebirth of the so-called yen carry trade when it froze after its rate hike last summer briefly crashed global stock markets. The NASDAQ, for instance, swooned 14% in a matter of days in late July/early August.

But while Japan’s central bank has been cowed into stasis, that hasn’t been the case with the long end of its bond market.

Power-puncher

As you can see, the yield on the 30-year Japanese Government Bond (JGB) is now over 2%. That doesn’t sound like much, because it isn’t, but this rate now exceeds the yield on China’s 30-year “govie”. It’s been at least 20 years since this has been the case.