Haymaker Daily

On earnings optimism

Hello, Subscribers:

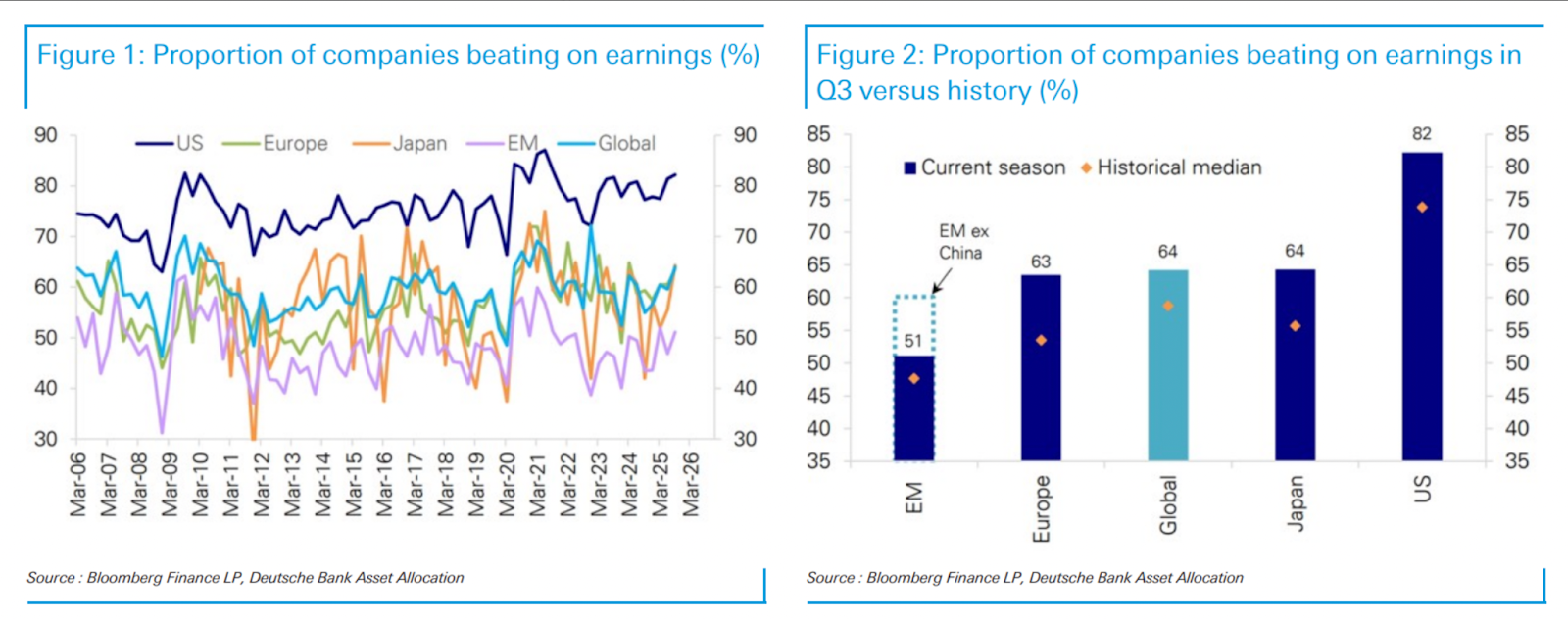

While there’s a healthy dose of doom and gloom in the markets (and these pages) of late, there are some reasons for optimism. With the bulk of Q3 earnings now behind us, over 90% of U.S. companies and more than half of their European and Asian counterparts having reported, the global earnings season has surprised to the upside.

Across the board, earnings beats came in at the top end of historical ranges. In the U.S., the breadth and strength of earnings growth stood out most, as two-thirds of S&P 500 companies reported double-digit profit growth, and sector participation meaningfully expanded. Even stripping out the usual tech and megacap suspects, median earnings growth ex-Mega Cap Growth and Tech jumped from 1.4% last quarter to nearly 7% in Q3.

Japan, too, posted a blowout 16% earnings growth rate, turbocharged by a weakening yen (yes, that would be the absurdly undervalued yen). Meanwhile, Europe’s headline numbers looked more muted at 2.5% y/y growth, but that masks weakness concentrated in Energy and Autos. Excluding those sectors, the continent’s corporate earnings have quietly marched higher since 2021.

Emerging markets (EM) may be entering their own earnings breakout phase. Q3 growth came in at 8.6% (near the top of the post-2024 range) even excluding the cyclical tailwind from semiconductors (read: Taiwan Sem, TSM; believe it or not, Taiwan is considered an emerging market). Consensus forecasts have responded in kind, with forward upgrades for 2026 now pointing to double-digit growth across regions: ~13% in the U.S., Japan, and EM; ~10% in Europe.

Notably, EM forecasts were bolstered by upward revisions to Korea and Taiwan (TSM again), while U.S. earnings expectations have clawed back to pre-“Liberation Day” (April) levels. Sales growth remained robust in the U.S. and EM, and margins across most markets held near cyclical or record highs. While Europe and Japan still lag in terms of forward optimism, the overall picture suggests a global earnings backdrop that’s less fragile than macro bears would have you believe.

How much of that growth upside is a function of feverish AI spending? That’s a valid question, particularly given intensifying suspicions that a massive over-investment in AI is occurring. That immense spending has definitely benefited a long-time Haymaker favorite, the aforementioned Taiwan Semiconductor.

David “The Haymaker” Hay

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions.

David Hay is a passive owner of Evergreen Gavekal (“Evergreen”), a registered investment adviser with the Securities and Exchange Commission. As of 03/31/2025 Mr. Hay has no involvement in the day to day operations of Evergreen, nor is he involved with any investment research, or investment management performed by Evergreen. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on an individual’s investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.