Haymaker Daily

On a half-century loan

Hello, Subscribers:

We’re not sure who said it first, but the maxim about taking Trump seriously but not literally remains good advice, for the sake of a tempered national conversation, if nothing else.

Regardless of your opinion of Trump, what’s indisputable his how he throws ideas out into the national conversation with little regard for a) how they will be received, b) their viability, c) if they sound at all politically wise, or d) what unintended consequences they might have on the industries, nations, populations to which they apply. There is always a phenomenon of disproportion in play when Trump speaks on matters of consequence. A quick, 40-syllable remark from Trump reliably turns into a mundane segment where legacy media explains (at great length) why whatever he said could never work.

And guess what? When it comes to the 50-year mortgage rate, they’re actually right. It’s a bad idea because it would stack more chips in the banks’ favor, would do little to reduce monthly payments, and ultimately fails to address the larger problems with housing affordability. The elephant in the room is a combination of inventory and rates, and that’s where Trump’s attention should really be.

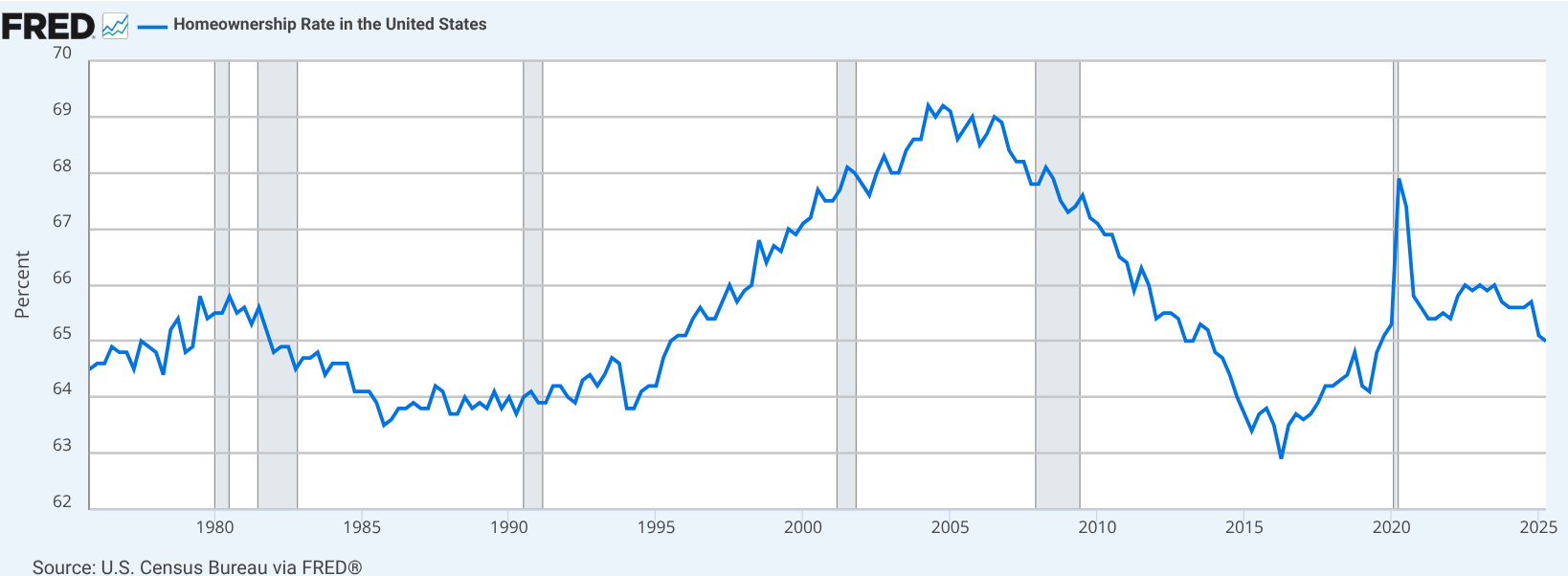

As you can see below, home ownership has been much lower in years past, but there’s no arguing that it’s doing particularly well at the moment. Potential buyers are either priced out, afraid to move before the promised land of lower interest rates re-appears, or simply can’t find what they’re looking for in their market(s) of choice.

To the extent that any government or Trumpian focus should be on mortgage duration, it should be in the other direction. How about working with banks on some incentives to provide 12-, 16-, and 20-year mortgages? Maybe foster a federal program that incentivizes first-time (or even second- and third-time) buyers to pay-off more of what they owe in the first five years. Maybe the banks won’t like that part, but they do like houses to change hands, and circulating real estate is good for them. Stagnation is, of course, much worse for business than financially prudent borrowers.

Whatever comes of Trump’s real-time, stream-of-consciousness brainstorming, the 50-year mortgage proposal belongs with New Coke, Joanie Loves Chachi, and Michael Jordan’s baseball career in the collective waste basket of social memory.

David “The Haymaker” Hay

IMPORTANT DISCLOSURES

This material has been distributed solely for informational and educational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. All material presented is compiled from sources believed to be reliable, but accuracy, adequacy, or completeness cannot be guaranteed, and David Hay makes no representation as to its accuracy, adequacy, or completeness.

The information herein is based on David Hay’s beliefs, as well as certain assumptions regarding future events based on information available to David Hay on a formal and informal basis as of the date of this publication. The material may include projections or other forward-looking statements regarding future events, targets or expectations. Past performance is no guarantee of future results. There is no guarantee that any opinions, forecasts, projections, risk assumptions, or commentary discussed herein will be realized or that an investment strategy will be successful. Actual experience may not reflect all of these opinions, forecasts, projections, risk assumptions, or commentary.

David Hay shall have no responsibility for: (i) determining that any opinion, forecast, projection, risk assumption, or commentary discussed herein is suitable for any particular reader; (ii) monitoring whether any opinion, forecast, projection, risk assumption, or commentary discussed herein continues to be suitable for any reader; or (iii) tailoring any opinion, forecast, projection, risk assumption, or commentary discussed herein to any particular reader’s investment objectives, guidelines, or restrictions.

David Hay is a passive owner of Evergreen Gavekal (“Evergreen”), a registered investment adviser with the Securities and Exchange Commission. As of 03/31/2025 Mr. Hay has no involvement in the day to day operations of Evergreen, nor is he involved with any investment research, or investment management performed by Evergreen. The information herein reflects the personal views of David Hay as a seasoned investor in the financial markets and any recommendations noted may be materially different than the investment strategies that Evergreen manages on behalf of, or recommends to, its clients.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this material, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on an individual’s investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

50 year mortgages would be a disaster for the borrowers just compare amortization schedules for 30 v 50. The problem also isn’t rates, unless you’re referring to the FED keeping rates at the zero bound from 2010-2023 with a tiny short-lived uptick once or twice during that period.

The problem is all that free money led to overconsumption of housing inventory and thereby bidding up housing prices. The current 10 year Treasury is about where it’s averaged for the last 50 years.