Friday Highlight Reel: Edition #7

A sampling of interesting observations from the Haymaker's network of market experts and favorite resources.

“Not many Feds have tightened into a financial crisis, let alone 11 straight months of decline in the official leading economic indicator.” -David Rosenberg, March 28th, 2023

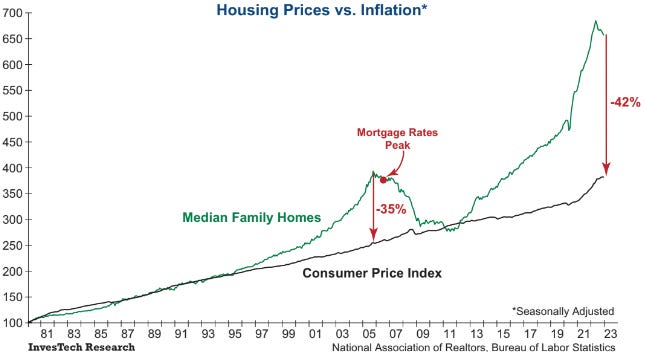

#1: Jim Stack of InvesTech Research on Housing and Inflation

“We have called today’s housing market the Achilles heel of the this economy, and that remains true despite a modest decline in home prices thus far. The graph below shows just how far housing prices could conceivably fall after their unprecedented ascent in recent years. Specifically, prices would have to decline an additional -42% from current levels to return to the broader inflation trend line, which far surpasses the dislocations that took place at the peak of the 2005 Housing Bubble…Given that housing is a major component of the economy and the consumer’s perception of wealth, a hard landing for housing would raise the likelihood of a much more severe recession.”

Haymaker Take: Jim Stack is among the rare breed of financial newsletter writers who also manages client money. From what I’ve heard and read, he’s done an excellent job of that over the years. Even though my email inbox is inundated with research from myriad sources, I recently signed up for Jim’s monthly newsletter. (Wow, publishing only once a month sounds like retirement to me!)

In a note late last month, Jim included the above visual, comparing home prices to the CPI over time. It’s a topic I touched on in my book, Bubble 3.0, and I went back even further than Jim. As you can see, his chart begins in 1980 but I found the same was true over even a longer timeframe — like about 100 years! From 1899 until 1999, U.S. home prices essentially tracked inflation. Something obviously changed in the late 1990s and it became very pronounced around 2002. This was when the Fed was being pressured by pundits such as Paul Krugman into creating another bubble to offset the drag from the bursting of Bubble 1.0, the tech mania. Unfortunately for the planet, the Fed caved into his urgings to inflate the housing market. It did so by cutting short-term rates down to a Great Depression-like level of 1%. It then left them there even as the economy robustly recovered from both the tech-wreck and the shock of 9/11/01.

The result, of course, was a financial calamity that almost crashed the global system. Most of us believed that, in its aftermath, we’d never see a repeat of that type of housing price inflation. Yet, as you can see, it’s even more extreme today. Moreover, as I’ve often written and said, the degree of overvaluation is far more egregious in many other Western countries, such as Sweden, Canada and Australia. Unsurprisingly, prices are falling at even a faster clip in those nations than they are in America.

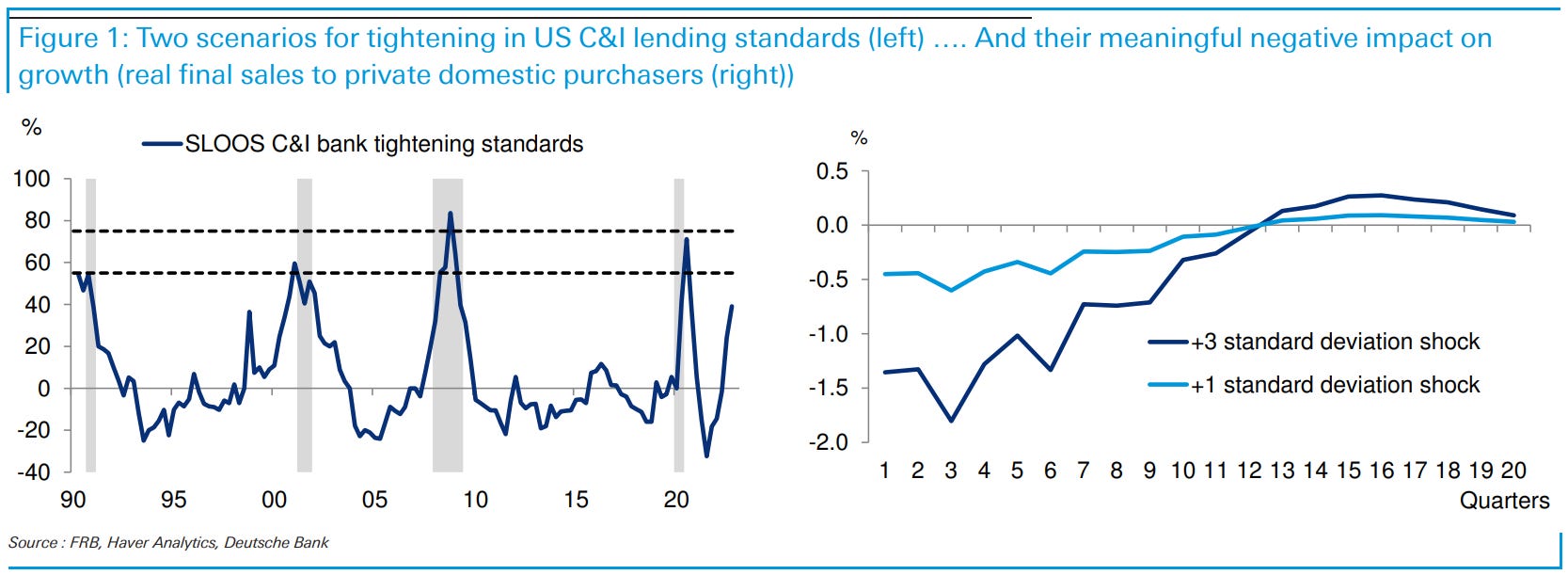

#2: Deutsche Bank’s Jim Reid on Tightened Lending

“The impact of the already tighter lending standards has always been a big part of (our team) being at the extreme end of the street in terms of our H2 2023 recession call, but this analysis shows the downside risks to this if the mini banking crisis does tighten lending standards further. Therefore the next Fed Senior Loan Officers’ Opinion Survey (SLOOS) that’s likely to be on May 1st or May 8th could be one of the most important datapoints of Q2.” (Emphasis added)

Haymaker Take: As you can see from the preceding chart on the left, the SLOOS C&I (Commercial and Industrial) bank tightening standards are already looking increasingly recession-like. The odds favor the SLOOS survey continuing to reflect increasing caution on the part of lenders. This is particularly the case as the banking industry’s cost of capital remains on a steep up-trend. A key driver of that is “cash sorting”, the shift of institutional and individual deposits out of near-zero-yield bank accounts into the much higher yields — and safety — of U.S. Treasuries. By the time the dust settles, I’m convinced several trillions will have been moved into government bonds and out of the banks’ freebie funding source. This trend, along with rising loan losses, is nearly certain to render the banking system an even stingier lender. One could quip right now that when it comes to economic momentum (or the lack thereof), “You SLOOS, you lose.”

#3: John Mauldin (Author of the uber-popular Thoughts From The Frontline) on Banking Best & Worst Practices

“I realize even relatively small businesses need liquidity for payroll and operations. Trust me, I’ve been there. But my accountants and bankers have always found ways to minimize that risk. It’s fairly simple to sweep excess amounts to a money market fund and bring it back as needed to clear checks. Keeping millions in the same bank just makes no sense. Yet it was common at SVB.

Nor is it just SVB. Even much larger banks can have more uninsured than insured deposits. This hasn’t always been the case. Here is a chart Ed Yardeni compiled comparing insured and uninsured deposits for all US banks.”

Haymaker Take: John is actually describing the “cash sorting” process mentioned in item #2. He’s spot-on that it is fairly simple. Yet it has astounded me how many businesses and people failed to take this Finance 101 action… at least until the recent bank blow-ups focused their minds. Accepting a far lower return for some degree of risk (uninsured deposits) is inexcusable.

As you can see from the Mauldin/Yardeni chart, this was a fairly recent phenomenon. The gap between the two lines was fairly modest prior to the pandemic response of sending out trillions of support payments to the private sector. For some strange reason, this money blitz mostly went into uninsured deposits despite their essentially yield-free status. A decade ago, there was more in insured than uninsured bank accounts.

My anticipation is that this will be the case again before long. If I’m right, that will amount to about $4 trillion, if not more, moving out of the banking system and into government securities where the deposit limit is irrelevant. As I’ve written before, this has negative implications for money velocity… and the economy at large. Even prior to the recent dislocations, bank deposits were falling at the faster rate in over 40 years.

To learn more about Evergreen Gavekal, where the Haymaker himself serves as Co-CIO, click below.

#4: Luke Gromen, author of Forest For The Trees, On Central Bank Policy

“What happened around early 2015? Something we have been harping on for the better part of eight years: For the first time in 40-50 years, global Central Banks stopped buying USTs on net. In 3q14, global Central Banks stopped sterilizing US deficits, instead putting their net surpluses into gold, with Central Banks cumulatively buying $307B (billion) in gold while selling nearly $500B in USTs on net.”

Haymaker Take: Luke Gromen is definitely one of my most important research sources these days. This is due, in no small part, to his focus on the looming threat of acute dysfunction in the U.S. Treasury bond market, arguably (but not much), the most important in the world. Unfortunately, very few other experts are running the numbers with Luke’s precision. Frankly, the math against a smoothly functioning bond market in America is becoming beyond worrisome.

For most of the past 50 years, foreign central banks were eager buyers of U.S. Treasuries as they recycled our huge and recurring trade deficits back into the dollar. But starting in the second half of 2014, that changed. This wasn’t a serious problem when the Fed was a buyer of trillions of U.S. “govies” via its serial QEs. (Officially, there were three iterations, beginning in late 2008, with an unofficial fourth version that began in September, 2019.) Now, though, the Fed is in the throes of Quantitative Tightening (QT), the antithesis of QE. This means that, in a bit over a year, the Fed has gone from a buyer of $1 trillion of Treasuries, on an annualized basis, to a seller of an equivalent amount. Combined with erupting deficits as tax revenues contract and support payments escalate — along with Social Security and Medicare Trust Fund selling, and the aforementioned foreign central bank dispositions — there could easily be $5 trillion of new Treasury debt that needs to find a home. To put that stunning number into some context, that’s the equivalent of about five Amazons, based on its current market capitalization.

#5: David Rosenberg, Canada’s Most Famous Economist, on Fed Cycles

“(Here) is the history of other financial and corporate failures, and just how long it took the Feds of yesteryear to respond with a series of rate cuts:

• Franklin National, October 1974 (the Fed eased that month)

• Penn Square, July 1982 (the Fed eased that month)

• Continental Illinois, May 1984 (the Fed switched from tightening to easing aggressively one month later)

• Lincoln Savings, April 1989 (the Fed eased two months later)

• Orange County, December 1994 (The Fed eased seven months later)

• Long-Term Capital, September 1998 (the Fed eased that month)

• Global Crossing, January 2001 (the Fed eased that month — intermeeting)

• Bear Stearns hedge funds, July 2007 (the Fed eased two months later)

• Repo market blowup, September 2019 (the Fed eased that month)

Every financial crisis came on the heels of an aggressive Fed tightening cycle. And they all mark the end of the rate-hikes and the onset of a series of cuts… and no fewer than three; far more when they involve recession. What made 1984 and 1994 special was that the economy was in the early-cycle phase, and the 1998 easings bought that expansion a lifeline that lasted little more than another year.”

Haymaker Take: It doesn’t take an imagination worthy of J.K. Rowling to visualize 2023 appearing on the above list in the not-too-distant future. As I write these words, the stock market seems to have decided this isn’t a financial crisis, after all. However, I doubt that conclusion will stand the test of time. Not with the potential for the U.S. government to overwhelm the bond market’s buying capacity, particularly as banks are likely to be reluctant to step up to the plate when deposits are fleeing en masse. (Admittedly, non-bank buyers will support the short-end of the Treasury market, such as with T-bills.) Additionally, with commercial real estate under intense pressure — and apartment buildings likely not far behind — banks are nearly certain to further curl up into the fetal position. Then, there is the popping of the global housing bubble which, by comparison, makes the Goodyear Blimp look like something a baseball player might blow in the dugout. The bottom line is that trouble is coming and, in many cases, has already arrived. Consequently, raising a bit more cash is a rational reaction to the latest bear market rally.

#6: Mike Rothman of Cornerstone Analytics on Crude Prices

“Over the past 25 years, crude oil prices have risen more than 4-fold and global demand grew by more than 33%. Just about every person reading this report has been taught that demand for a commodity goes down by varying degrees when its price rises (i.e., price elasticity has a negative coefficient). In the case of global oil demand, we have a case of perfect inelasticity.”

Haymaker Take: In my view, no one tracks the oil market as closely, or accurately, as Mike Rothman. For example, over many decades he’s gone up against the formidable (though highly fallible) International Energy Agency (IEA), challenging its chronic demand underestimation and typical supply overestimation. Thus far this year, he is predictably on-the-mark while the IEA is in its familiar omelet-on-its-face position, having once again whiffed on both supply and demand. His above stat on demand inelasticity seems to contradict the basic laws of economics. However, an alternative explanation speaks to oil’s essentiality, even as prices move higher. With current crude quotes, adjusted for inflation, well below where they were in 2006 — and immensely lower than their 2008 peak (unadjusted) of $140/barrel — Mike’s forecast of another oil-price surge this year seems eminently credible. The fact that speculative positioning is extremely depressed right now is another reason why energy investors should be putting on their rally caps. (The last time speculative longs were this depressed was in January, 2016, on the eve of a prodigious energy rally.)

#7: Cornerman Entry — MJM on Recent AI News

Some or most of you may know me as the Haymaker “Cornerman” and occasional contributor. Few of you, I’d guess, are aware that I recently launched my own Substack page (Opinions Impending) with the aim of focusing primarily on politics. As it happens, I’ve instead been almost exclusively focused on AI since the page launched. Given what’s been going on in the space this week, I thought you might like to add a dose of AI philosophizing to your financial analysis uptake.

Hope you enjoy.

-MJM

If there is more to sell and fewer buyers, does that mean interest rates need to go up? So avoid buying longer duration treasuries