Compliance: My Weekly Tightrope Act

(With your help, good things await on the other side)

“It is literally true that you can succeed best and quickest by helping others to succeed.” -Napoleon Hill

As we all know (though don’t really like), life is full of tradeoffs. This newsletter is a classic case of that. One of the most important attributes I bring to Haymaker editions is over 44 years of investment experience, including being Evergreen Gavekal’s Chief Investment Officer, now Co-CIO, for more than two decades.

Our firm is fortunate enough to now manage over $4 billion of client assets. We do so in a much different way than the majority of our esteemed competitors because we perform intensive research into individual securities. Most of our peers, but certainly not all, have moved away from actual asset management. The majority either farm out the process to firms like ours, or increasingly (often exclusively) utilize ETFs and other index solutions.

We are also willing to invest anywhere in the capital structure of a given company to achieve the best return relative to the risk involved. Our focus on high-income securities is also rare and we often find more attractive risk/reward characteristics with bonds and preferreds than on common stocks. As I’ve conveyed in the past, the performance of our bond- and yield-oriented equity portfolios has been much more than respectable.

Frankly, very few of my financial newsletter writing colleagues also manage money. While I’m convinced that this gives me significant advantages when it comes to providing investment guidance — particularly due to our talented research team — there is a downside. That would be the above-referenced tradeoff.

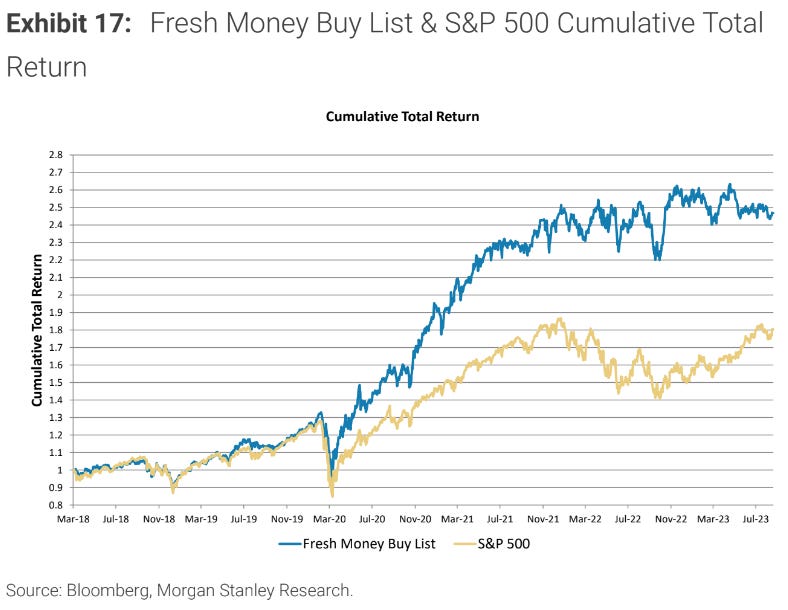

In my case, I need to be careful about how specific my investment recommendations can be with individual securities. This is primarily for compliance reasons and as a function of tightening SEC regulations. (It does continue to baffle me that many of our competitors don’t seem to have the same degree of restrictions. For example, one of my favorite Wall Street strategists, Morgan Stanley’s Mike Wilson, publishes a weekly Fresh Money Buy List. He also tracks its performance. Apparently, Morgan can do this because they have a retail brokerage arm and a money management division, but that doesn’t make sense to me.)

However, I can be very clear on my asset allocation calls. Frankly, I feel that’s how I provide the most benefit to Haymaker subscribers, along with my income suggestions (where I do have to be more guarded). For example, I put out a rare aggressive buy recommendation on the energy sector in our June 23rd Haymaker. (As regular readers are aware, I generally recommend dollar-cost-averaging into a position.) Since then, oil has vaulted 25% and the oil-and-gas producer ETF (XLE) is up 18%. (It is somewhat surprising to me the XLE hasn’t risen more than oil, but I’m not complaining.)

Going back to last year, I put out a buy on the oil service ETF. Oddly, when I did, the most pushback I received was from a couple of individuals who were actually in that industry. They warned me that I didn’t understand how bad conditions were in their field. Maybe I was just lucky, but that ETF has rallied significantly since then. Part of my logic was how cheap the stocks were trading at the time. Additionally, I was convinced that we were in the midst of a new upcycle for oil and natural gas prices. That was likely to stimulate demand for oil field service companies like Schlumberger.

Schlumberger (SLB)

Fortunately, that’s how it worked out and I continue to believe we are in a long-term bull market for energy securities. (One reason for our energy-related success is, in my opinion, a function of subscribing to a firm’s research I have long believed provides the best intel on the oil market: Cornerstone Analytics. It’s a very pricey service, but there’s no doubt in my mind it is worth the cost.)

We’ve also made timely endorsements of the midstream energy (pipelines) sector, gold miners when they’ve been down, and uranium after it dipped this summer (prior to a robust rebound). We’ve suggested ETFs that invest in these as the most diversified ways to capitalize on their healthy fundamentals. Further, we did suggest trimming into the gold miners’ periodic rallies, particularly in my predecessor newsletter (EVA), back in 2020, but also in January of this year (about 14% above where they are trading currently).

Admittedly, these all have a hard asset orientation. That’s befitting one of my overarching investment positioning suggestions: to focus on asset classes that possess an intrinsic scarcity aspect. However, this newsletter has also given timely suggestions about avoiding long-term Treasury bonds that have been struggling since the inception of the Haymaker publication.

Additionally, for any subscribers with meme-stock exposure (GameStop, AMC, Carvana, to name a few), our repeated warnings about the shocking disconnect between very poor fundamentals and gone-postal stock prices were timely. We even proposed that some might want to short or buy puts on these lottery-ticket-like names. As usual, I put my personal capital on the line by betting against them in my long/short account. (More on one of the above in the Down For The Count section, for paying subscribers.)

Most of our other negative ratings were well-rewarded, though a big whiff, so far, has been TSLA. My negativity toward the U.S. dollar was another call that was off-the-mark, as I’ve repeatedly conceded.

In last week’s Champions section for our paid-up readers, we introduced another bond idea, though with oblique references to the specific name. However, we did provide an update on an income highlight from a few weeks back that was fairly direct.

Some readers have actually taken action on our suggestions. One, who is also a client, recently emailed me that he generated a sizeable gain on a uranium play thanks to my repeated bullishness on U308.

Another client and Haymaker reader made an excellent point. In his case, he runs most of his money on his own. To help him in that regard, he subscribes to a number of newsletters. He recently wrote me that it only takes one good idea per year to justify the cost.

My goal is to provide our paying subscribers with lot more than one good idea per year. This is even after taking into account the inevitable suggestions that don’t work out well. It wasn’t too long ago uranium was in that category before it (figuratively) caught fire since mid-April.

It’s only fair to those who help us cover the cost of our service that they get the most guidance. This is particularly the case with our top-tier Founding Members. (If you’d like a sneak preview of that suite of service, please let us know.) Frankly, we need your help by either signing up for paid status or recommending the Haymaker publication to your friends and family, or both.

Thank you!

David “The Haymaker” Hay

A Note to Founding Members: Mark Your Calendars!

David will be hosting our next Haymaker Dialogues Live Webinar on September 28th (time to be determined). Thanks to all of you who made the first session such an engaging experience!

To all other subscribers reading this, the Haymaker Dialogues are a presentation-focused production which include macro research and sector-specific analyses, delivered by David, followed by an open Q/A session in which every attendee is welcome to ask the host anything they’d like on markets, economics, and even particular securities. We offer our Founding Members a couple of perks, but that’s the real monthly highlight.

Become a Founding Member today and we’ll see you on the 28th!

-The Haymaker Team

Bonus Charts (These Two Sourced from Morgan Stanley)

Not yet a paid Haymaker subscriber? Complete the brief survey linked below and we’ll set you up with a 90-day trial at no cost.

Champions - An Anti-Depressant For Your Portfolio

Based on the epidemic of depression in America these days, you would think there would be strong demand for lithium (Li) for that reason alone. When you add in the fact that the consumption of Li is going ballistic due to the rapid growth by electric vehicles (EVs), you might also come to the conclusion that the stocks of publicly traded producers of this critical green energy commodity would be near all-time highs. Further, you might assume their P/E ratios would be lofty, particularly when considering the inflated prices at which many chronically unprofitable companies are trading (again!).

Yet, despite the exceedingly supportive conditions for the Li sector, a leading U.S. producer is trading at a mere 11 times its estimated earnings for this year. Based on consensus projections for 2024, it is quoted at an even more modest P/E of 9. There is a decent chance it can earn considerably more next year than the mean estimate of $2.37.

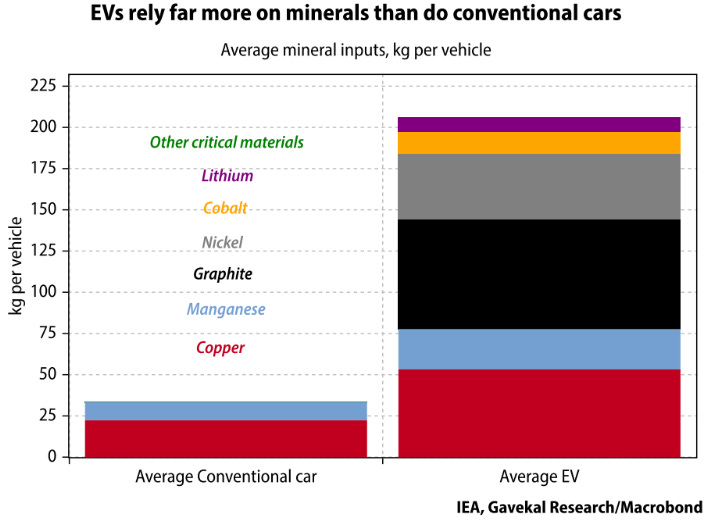

This newsletter has repeatedly endorsed copper stocks due to the fact that EVs consume three to four times more of the red metal than do traditional Internal Combustion Engine (ICE) cars. In the case of lithium, ICEs don’t use any at all. While it won’t be included to the degree of copper in EVs, the increase in demand will for Li will be extremely significant.

According to the astute folks at Sprott, as of year-end 2022, there were over 26 million EVs in the global auto fleet. The International Energy Agency (IEA) is forecasting that number to rocket to 350 million vehicles by 2030. The Sprott team believes Li supply will need to increase 16% to 20% annually to satisfy the demand surge.

As with so many critical Great Green Energy Transition materials, developing new mines to meet the surging usage is exceedingly difficult. For example, one of America’s most promising deposits, outside the tiny Nevada town of Tonopah (ironically, that’s the same location as AMC Entertainment’s ill-fated gold mine, Hycroft). Hopes are high that in a few years this will be an important source of U.S. Li supply. However, NASA is intervening due to the fact that it uses the bright white Li deposits to calibrate satellites. Apparently, the most promising portion is at risk of being blocked. At a minimum, NASA’s actions are likely to delay this project.