Friday Haymaker

A Note from Gavekal's Will Denyer

“Economics is a highly sophisticated field of thought that is superb at explaining to policymakers precisely why the choices they made in the past were wrong. About the future, not so much.” -Ben Bernanke

The Recession That Never Was…

The classic preconditions of a recession have long been in place. Two of the most prominent have been the inverted yield curve (short interest rates higher than longer-term rates) and the steadily declining, except for one month, Leading Economic Indicators (LEIs). Both have been flashing red for two years. In the case of the yield curve, the inversion has been the longest on record.

With the LEIs, the downtrend has been running for 28 months. However, a slight increase in February broke what had been a 23-month streak of consecutive down months. That stretch exceeded even what led up to the Great Recession.

On the positive side, the trailing six-month rate of decline eased in the second half of last year, indicating diminished risks of an actual contraction. But this implies the LEIs were quite weak in the first half of 2023. That, and other warning signals, such as last year’s banking crisis, led many to conclude that the odds of a recession happening last year were high. The Haymaker team was among the worrywarts.

The fact that there was also a lengthy yield curve inversion seemed to clinch the call. Historically, this indicator alone has had a 100% recession predictive success rate, at least when the inversion has been long lasting versus brief. Yet, 2023 actually turned out to be a year of solid GDP growth, coming in at 2.5% in real, or inflation-adjusted, terms. So, what gives? Or, perhaps more accurately, what gave the economy such remarkable resilience?

Today’s Gavekal Haymaker, authored by its monetary and macro-economic maven, Will Denyer, examines one of the primary factors behind that surprising buoyancy. It should come as no surprise to regular Haymaker readers that the effective doubling of the federal deficit (using proper accounting), from one trillion to two trillion in the government’s fiscal year ending 9/30/23, provided enormous economic lift. (Will, however, contends it was much less than most — like Luke Gromen and the Haymaker — believe.)

Fiscal year 2024 was supposed to be a different story. Until last month, the Congressional Budget Office (CBO) was projecting this year’s deficit to actually contract, though to a still outlandishly bloated $1.5 trillion. This brought up the old debate about stock vs flow. In other words, is what really matters the total stock of red ink (the level of the deficit) or the rate of change (the flow)? If it’s all about the stock, then the government’s shortfall remains highly stimulative. However, if the flow is the key consideration, then one could argue it’s an economic headwind.

This controversy became somewhat moot on June 18th when the CBO upped its forecast for the 2024 deficit by $400 billion to $1.9 trillion, as Will discusses. This amounts to 7% of GDP which may actually exceed 2024’s growth in nominal (i.e., including inflation) economic activity. Said differently, if you back out the deficit from nominal GDP, the economy might actually already be contracting.

But this is where Will’s note provides some unique insights. A big driver behind this year’s return to the $2 trillion deficit range is the exploding cost of financing that immense shortfall. This is because maturing Treasury bills, notes, and bonds are rolling over at much higher interest rates. The interest tab is basically doubling from around $500 billion to $1 trillion. This means that the “primary deficit”, which excludes interest, is “only” around $1 trillion.

Will contends it’s the primary deficit that is what really counts when it comes to stoking or retarding economic expansion. He explains his reasoning in more detail but the basic idea is that sending interest payments to rich people, who hold most of the T-bills, doesn’t juice the economy as much as spending on defense or the green energy build out. (One could certainly argue about the long-term economic benefits of such spending but, in the here and now, they do provide a boost.)

Personally, I’m not as convinced that injecting $500 billion more from interest payments doesn’t create a hefty amount of stimulus. But I certainly agree it’s much more skewed to high-end consumers and, of course, the mega-tech companies that sit on massive cash holdings. For the less affluent and more indebted (both corporate and consumer) it’s very much a case of anti-stimulus.

The bottom line is that the flat year-over-year deficit is no longer an economic amphetamine. Based on Will’s analysis, it may even be a drag, at least on a comparative basis to 2023. Accordingly, this is another reason to expect the long-delayed recession to be close at hand.

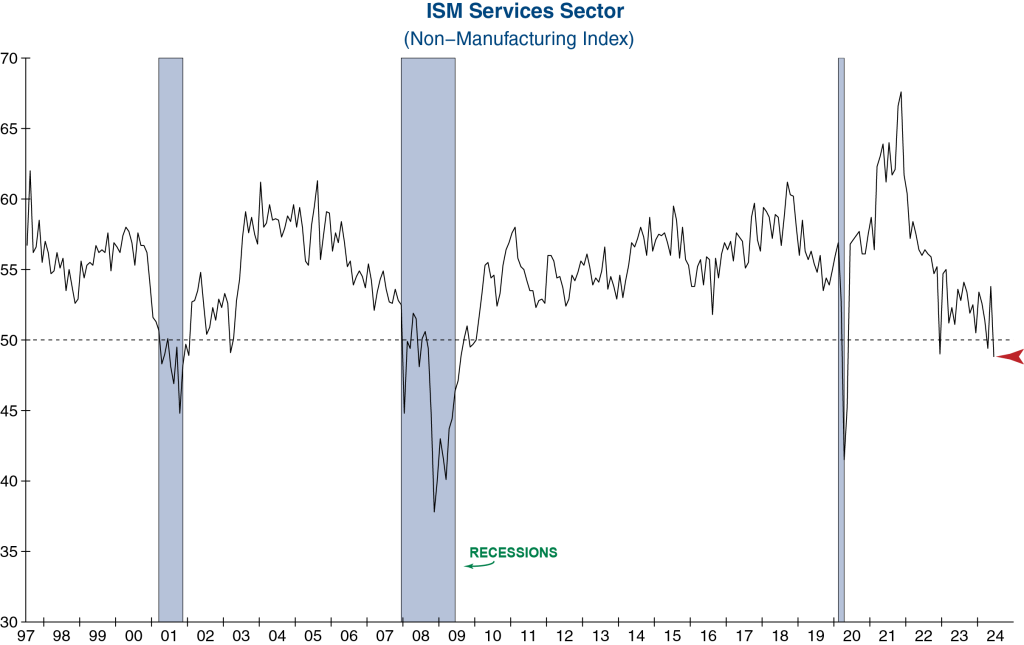

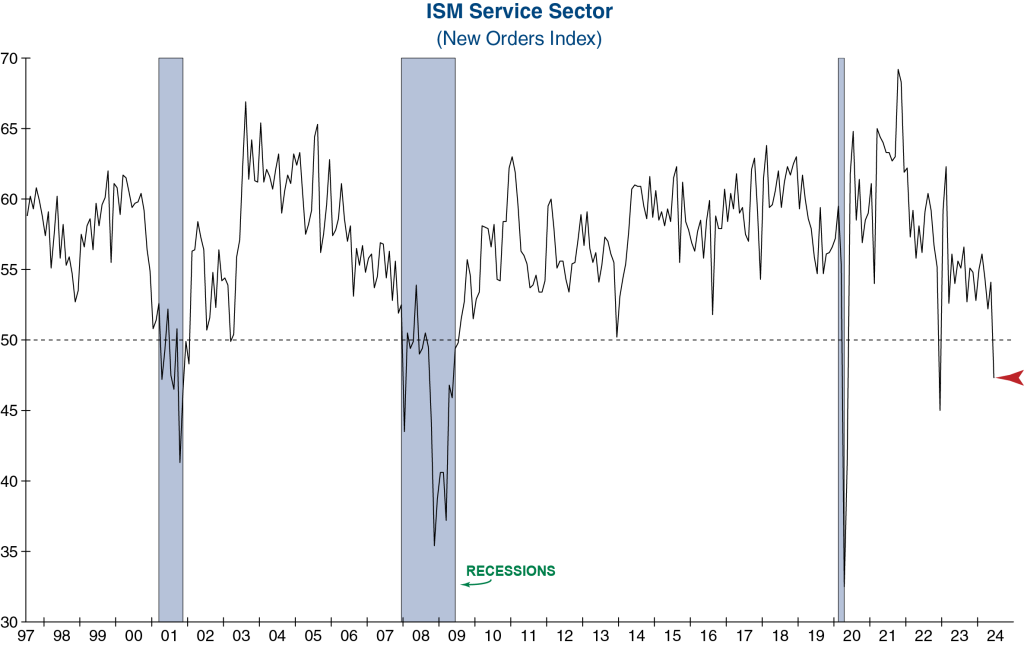

On Wednesday, I had a phone call with Danielle DiMartino Booth. If you don’t know, she’s staked her reputation on her forecast that a downturn is already underway. The array of weak data released that day — especially the profoundly weak Non-Manufacturing (Services) Purchasing Managers Index — only strengthens her convictions. In support of her stance, the softness in this, and New Orders, almost never occurs outside of recessions.

She also told me the official payroll census data from the third quarter of last year has revealed net job losses back then, not the supposedly strong employment growth originally reported. (Frankly, I haven’t seen that and couldn’t find it on a search, though I trust her accuracy.) Danielle expects that will also be the case with the fourth quarter.*

She further expressed her concerns about the (Not So) Great Debate. She isn’t a fan of either candidate, but she worries Joe Biden’s appalling performance sets the stage for a potential Red Wave come November. Realizing that most Haymaker readers likely find that to be a pleasant prospect, her fear is that an unchecked Trump Term 2.0 will unleash “yuge” tax cuts and unbridled spending (my note: instead of just unbridled spending under Biden).

This could create a bond market crash, similar to what happened in the UK in 2022, as we have also postulated in these pages. Justifying her concerns, the Treasurys have been on their heels since the debate debacle, despite the raft of punk economic releases. Suffice to say another bond market rout, similar to what we saw last fall, is not a favorable development for a priced-for-perfection stock market.

Consequently, it’s another reason for investors to deeply reflect on one of Warren Buffett’s favorite dictums: “Be fearful when others are greedy and be greedy when others are fearful.” Right now, greed is running wild. And, contrary to Gordon Gekko’s mantra, at a time like this, greed is definitely not good.

The Haymaker Team

*The closely followed Non-Farm Payroll report was released this morning and, superficially, it looked healthy. However, once again, revisions to previous months were decidedly down. Between April and May, 111,000 fewer jobs were created than previously reported. Accordingly, today’s overall report was not robust. Additionally, the unemployment rate rose to 4.1%, up about 0.7% from the low. This increase in joblessness is approaching a level that has been consistently accurate in forecasting prior recessions.

A Shifting US Fiscal Dynamic

Will Denyer (Originally published June 25th, 2024)

The US economy grew faster than expected last year, in part because it got a solid fiscal boost. In 2024, that extra demand will be less pronounced, which is one reason to expect slower growth this year. Such an assertion may surprise those who just read headlines about US deficit exploding to US$1.9trn in the 2024 fiscal year, but that is the total deficit. From a near-term growth perspective, what matters more is the primary deficit (excluding interest costs), which is projected to flat-line this year. Looking ahead, the direction of fiscal policy will be decided in November’s general election—with relatively clear implications for financial markets, and less clear implications for deficits and growth.